A view of the construction site of Jeddah Tower in Jeddah, Saudi Arabia, January 20. (REUTERS/Ibraheem Abu Mustafa)

The conflict between Iran and Israel had an immediate impact on financial and commodity markets. Stock markets moved lower and oil prices spiked higher as investors fretted about the potential implications for the flow of oil from the Middle East. Stock markets have subsequently recovered most of the lost ground, but oil prices have remained elevated at around $75 per barrel for Brent crude. If the conflict does not escalate further, the impact on the Saudi economy will be small and potentially positive. If the conflict spreads and affects shipping in the Strait of Hormuz, Saudi oil facilities, or business and consumer confidence, the impact will be negative and more significant.

State of Play – Saudi Economy in Good Shape

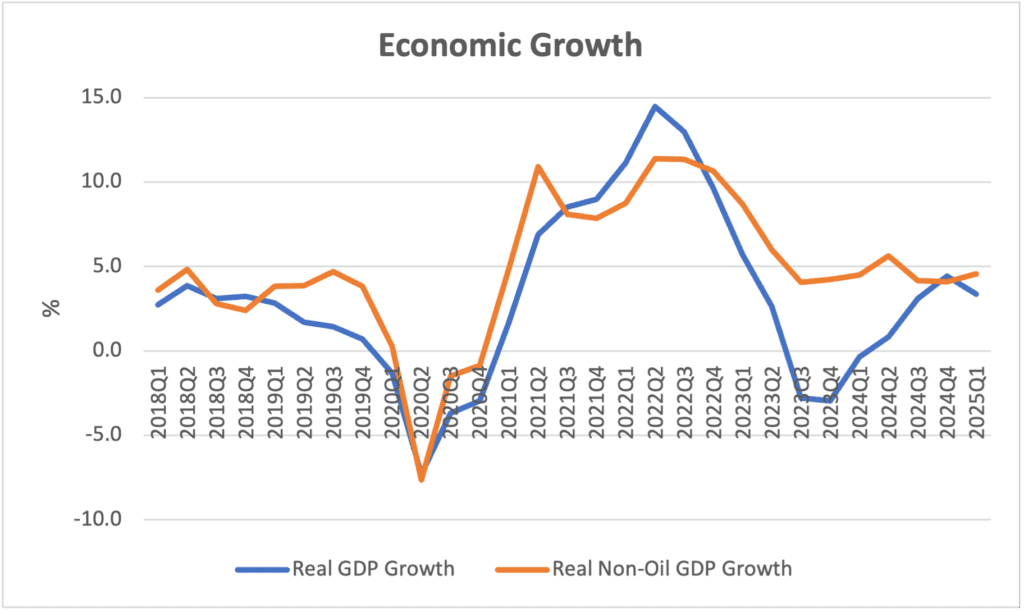

Prior to the outbreak of hostilities, the Saudi economy was doing well, albeit with the prospect that non-oil sector growth would slow as the year progressed. According to the gross domestic product data published by the General Authority of Statistics, the non-oil economy grew by 4.6% (year-on-year) in the first quarter of 2025, underpinning growth in the overall economy of 3.4%. The rate of non-oil growth was in line with the average of the preceding six quarters. Investment and consumption spending both grew strongly, with a notable increase in investment in the oil sector in line with Aramco’s announced capital spending plans. The retail, wholesale, restaurants, and hotels category contributed significantly to growth, consistent with strong private consumption, as did the manufacturing sector.

Source: General Authority for Statistics

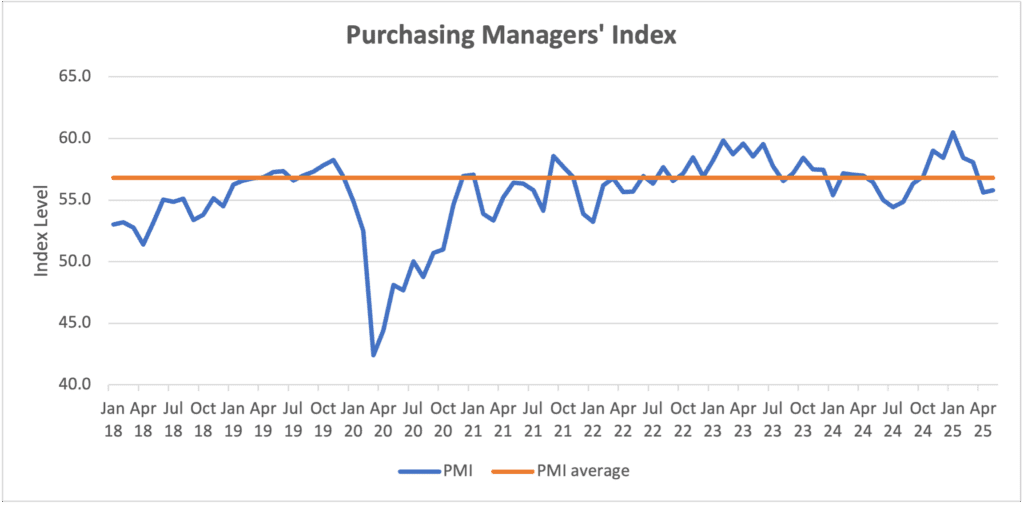

The GDP data for the second quarter will not be published until late July, but several monthly indicators can help track the path of the economy on a higher frequency basis. While these indicators do not paint a clear picture, on balance they suggest a modest slowdown in the non-oil sector is underway. The Purchasing Managers’ Index, a monthly survey of business confidence published by Riyad Bank, has declined since the turn of the year and in April and May dipped below its long-term average. There has also been a sharp drop in new construction contracts issued this year according to data collected by MEED and the Saudi Contractors Authority, while point of sales transactions (an indicator of retail sales) have slowed to their weakest level since the coronavirus pandemic. Nevertheless, bank lending to the private sector (a broad economic bell weather) and cement sales (another indicator of construction activity) have accelerated in recent months casting some doubt on the slowdown story.

Source: Riyad Bank

While there is uncertainty about the current direction of the non-oil economy, there is no doubt that growth in the oil sector is accelerating. OPEC+ has moved more quickly than expected to reverse its earlier production cuts. Saudi Arabia is a major beneficiary of this move. Oil output will rise to 9.5 million barrels per day by July compared to an average 8.9 mb/d in the first quarter of the year. Even if the OPEC+ alliance decides not to increase production further during the rest of the year, crude oil production would still be 3.9% higher in 2025 than in 2024.

Regional Conflict and the Saudi Economic Outlook

Before the conflict, a reasonable baseline for the Saudi economy was that real GDP would grow by around 3.5% in 2025 compared to 2% in 2024. Real non-oil GDP growth could be expected to slow to between 3% and 3.5% (4.6% in 2024) if the government cuts spending to meet its budget target and the Public Investment Fund slows project implementation. Real oil GDP would grow by close to 4% (-4.3% in 2024) given the actions by OPEC+. The fiscal deficit would be around 4.5% of GDP and the current account deficit around 4% of GDP (both assuming an oil price of $65/bbl).

Oil prices and oil production will be the most important and immediate channels through which the conflict impacts the Saudi economy. Higher oil prices are good news for the budget, current account balance, and growth. A sustained $10/bbl increase in oil prices would result in a $20 billion increase in fiscal revenue over a full year. If the conflict leads to a decline in Iranian oil exports, other OPEC+ countries could have the opportunity to further accelerate their production increases, with positive fiscal, current account, and growth benefits. A 300,000 b/d increase in oil output sustained over a year would boost fiscal oil revenue by around $5 billion. Combined, these two effects could reduce the forecast fiscal deficit by around 2% of GDP. Other channels through which the conflict could affect the economy are business and consumer confidence and tourism inflows. The impact on these factors is difficult to judge but unlikely to be significant if the conflict remains contained. All in all, real GDP growth could be about 1 percentage point higher, mainly due to the higher oil output.

A broadening of the conflict would more significantly change the economic outlook for Saudi Arabia. Attacks on Saudi oil facilities (unlikely given the improved relations between Riyadh and Tehran in recent years) or disruptions to shipping in the Strait of Hormuz could at least temporarily reduce oil production and exports even if some oil can be sent via pipeline to Yanbu on the Red Sea coast and shipped from there. A hit to oil production or exports would lower growth, but oil prices would also undoubtedly surge higher in such a scenario. The overall impact on oil revenue, and therefore the fiscal and external balances, is therefore difficult to judge and would depend on the relative strength of the impact on oil prices and production/exports. More generally, business and consumer confidence would be negatively affected, foreign investors would be deterred by the instability in the region, and overseas visitors would likely stay away given safety concerns. These effects would all reduce growth in the short term and could have longer-lasting effects if investors reassess the longer-term risk environment and hold back on the foreign direct investment flows that are needed to support the Vision 2030 reforms.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

AGSI explains what Israel’s sudden and massive attack on Iran is likely to mean for Gulf Arab states, Iran, the United States, and global and regional economies.

Saudi Arabia has continued to make progress in diversifying its economy, although lower oil revenue, higher imports, and stronger remittance outflows pushed the current account into a small deficit in 2024.

If the memorandum of understanding between the United States and Iran holds, the Saudi economy will grow strongly in the second half of 2026 and into 2027.

The Saudi budget recorded a large deficit in the first quarter of 2026 as spending surged, but higher oil revenue during the rest of the year should limit the size of the annual fiscal deficit.

Business conditions in the Gulf generally improved in April, but they remained weaker than before the Iran war. There are signs that price pressures are increasing as the conflict impedes trade.

On January 8, AGSI hosted a virtual roundtable with its leadership and scholars as they look ahead and assess trends likely to shape the Gulf region and U.S. foreign policy during the coming year.