The Iran War and the Saudi Economy

Data shows that the Saudi economy is being negatively affected by the U.S.-Israeli war on Iran, and the impact will likely continue for the next few months at least.

Previously released data on oil production and business confidence had forewarned that a slowdown in Saudi economic growth was imminent. Saudi oil production fell to around 7 million barrels per day in March from 10.9 mb/d in February (OPEC data), as exports were curtailed by the closure of the Strait of Hormuz. The Riyadh Bank purchasing managers’ index, a monthly measure of business confidence, fell to its lowest level in March since the early days of the coronavirus pandemic. The index has proved in the past to be a useful leading indicator of the non-oil economy. A business confidence index published by the Saudi statistics authority fell in March to its lowest level since it was first published in 2023.

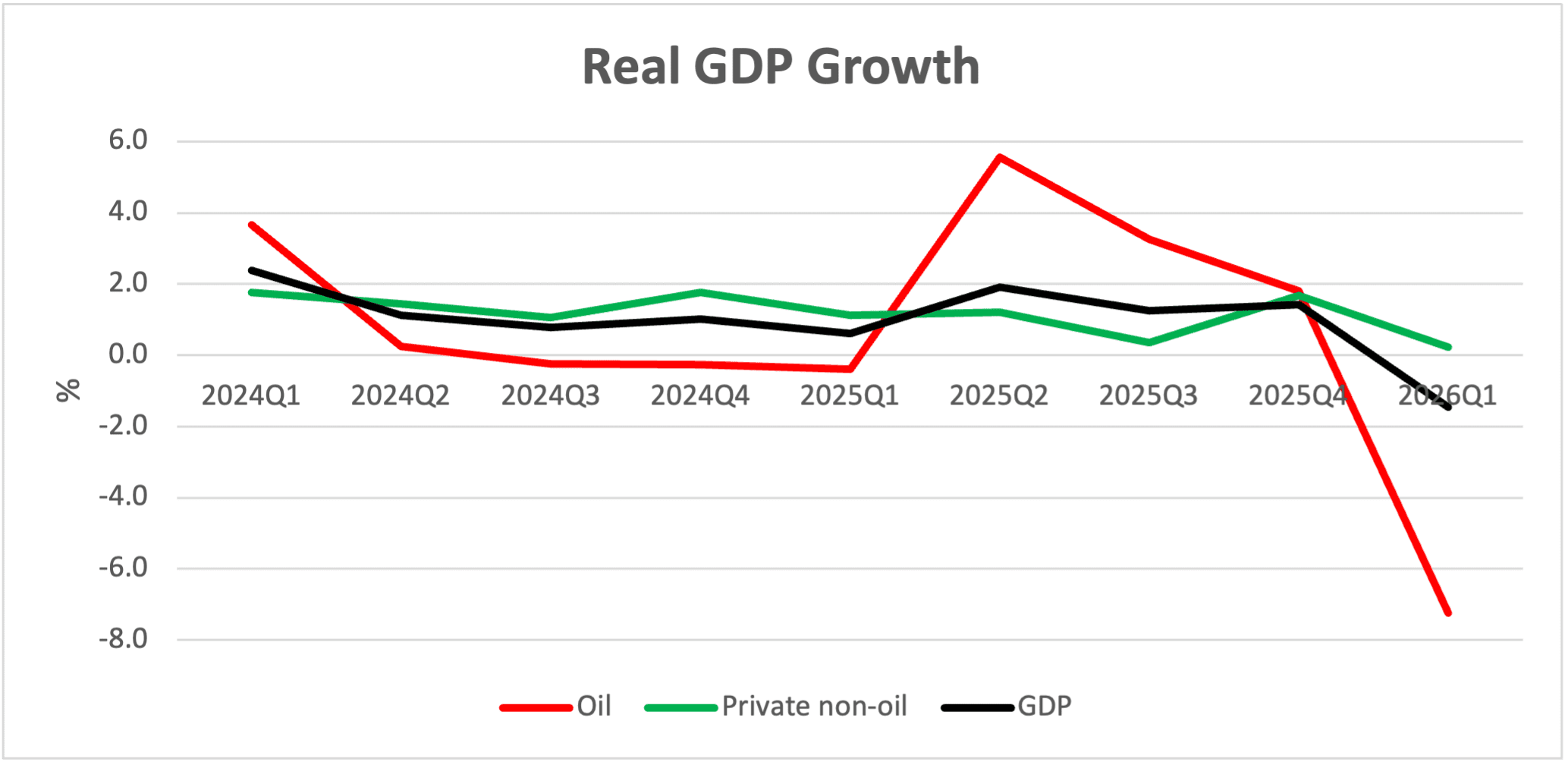

The growth slowdown was confirmed with the release of the “flash” or preliminary estimate of gross domestic product for the first quarter of 2026. Real oil GDP is provisionally estimated to have contracted by 7.2% (quarter on quarter, seasonally adjusted) compared to average quarterly growth during 2025 of 2.6%. Growth in real private sector non-oil GDP slowed to 0.2% (quarter on quarter, seasonally adjusted) compared to average quarterly growth during 2025 of 1.1%. Overall real GDP contracted by 1.5% (quarter on quarter, seasonally adjusted) compared to average quarterly growth of 1.3% during 2025. The year-over-year growth rate of real GDP slowed to 2.8% in the first quarter of 2026 from 5% in the fourth quarter of 2025.

Source: General Authority for Statistics.

Note: Chart shows the quarter-on-quarter percent change of the seasonally adjusted series

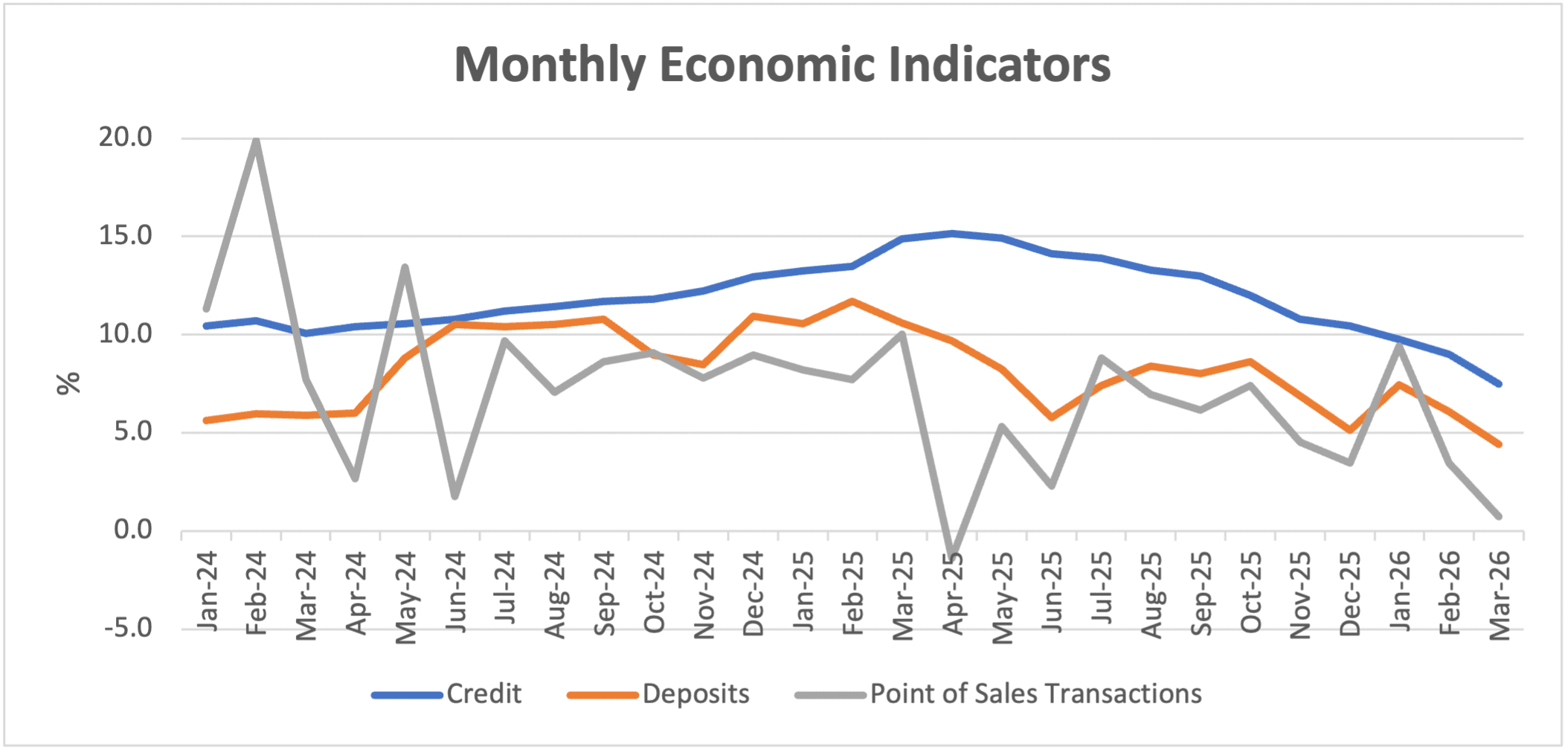

While the drop in oil output can be fully attributed to the effects of the conflict, non-oil growth was slowing before the war started, and disentangling the impact of the war from other factors, such as the pullback in government and Public Investment Fund spending, is very difficult. Monthly indicators of non-oil activity generally do not show a significant change in behavior in March. For example, while the growth rate of bank lending to the private sector slowed in March to 7.5% (year on year), this simply continued a trend that has been underway since mid-2025. Similarly, the growth in the deposits that individuals and businesses hold at commercial banks slowed to 4.4% (year on year) in March, but this continued the trend since early 2025. Point of sales transactions, a proxy for consumer spending, did slow quite sharply in March, but this series tends to be quite volatile month to month. Last, the Ipsos consumer sentiment survey dipped slightly in March, but this took the index only back to its level in late 2025. Indeed, comparing this index to the purchasing managers’ index suggests that consumers are much less concerned about the implications of the conflict than businesses.

Source: Saudi Central Bank; author calculations

Note: Chart shows year-on-year percentage change of each variable

Difficult Months Expected Ahead

The Saudi economy is likely to contract sharply in the second quarter of 2026, largely due to the oil sector. While the East-West oil pipeline has allowed Saudi Aramco to export some 4 mb/d to 5 mb/d from the port of Yanbu on the Red Sea coast, this does not fully cover for the loss of access to the Strait of Hormuz. Consequently, Saudi oil production will remain well below preconflict levels until a credible plan to safely reopen the Strait of Hormuz is in place and oilfields where production has been cut are brought back to full operating capacity. If oil production is in a range of 7 mb/d to 7.5 mb/d during April-June, this would imply a contraction in real oil GDP in the second quarter of 2026 of between 19% and 25% relative to the first quarter.

The outlook for the non-oil economy is more difficult to predict. Given that Iranian attacks on infrastructure have paused with the cease-fire, it is likely that business confidence will rebound in April, although a recovery to preconflict levels is unlikely until the threat of renewed hostilities is completely removed. A renewal of hostilities, on the other hand, would push business confidence back down in May and subsequent months. In the absence of job cuts or a pickup in inflation, consumer confidence and spending may prove quite resilient for a while longer. At this stage, a best guess would be that real non-oil GDP growth will follow a similar path to that during the first year of the coronavirus pandemic – a contraction in the second quarter followed by a rebound in the third quarter (providing the hostilities have ended by then).

To understand how the economic situation is evolving in Saudi Arabia, an eye should be kept on several important upcoming data releases. Of particular interest are the Riyadh Bank purchasing managers’ index for April (released May 5), Aramco’s first quarter earnings report (May 10), the government’s budget performance report for the first quarter (around mid-May), and international trade data for March (May 25).

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

Related

Saudi Economic Spotlight

Apr 2, 2026

Saudi Equities Outperform Global Markets

Saudi equity prices have risen since the start of the Iran conflict, outperforming many regional and global markets. Whether this continues will depend on how and when the conflict ends.

The Saudi Fiscal Deficit in 2025 Was Larger Than Expected

The 2025 budget deficit was larger than expected. The 2026 deficit is also likely to exceed the budget target, but higher oil prices may help contain any overrun.

Putting the 2026 Saudi Budget Under the Microscope

The Saudi government projects that the budget deficit will narrow during 2026-28, but this will depend on a rebound in oil prices and tight control of spending.

Apr 2, 2026

Saudi Equities Outperform Global Markets

Saudi equity prices have risen since the start of the Iran conflict, outperforming many regional and global markets. Whether this continues will depend on how and when the conflict ends.

The Saudi Fiscal Deficit in 2025 Was Larger Than Expected

The 2025 budget deficit was larger than expected. The 2026 deficit is also likely to exceed the budget target, but higher oil prices may help contain any overrun.

Putting the 2026 Saudi Budget Under the Microscope

The Saudi government projects that the budget deficit will narrow during 2026-28, but this will depend on a rebound in oil prices and tight control of spending.

Analysis

Have Saudi Labor Market Reforms Run Their Course?

Recent data suggests that the positive impact of a decade of reforms to improve Saudi labor market outcomes may now be waning.

Saudi Arabia Weathers the Iran War Thanks to Investments in “Economic Resiliency”

The impact of the Iran war on the Saudi economy has been mitigated by investments in “economic resiliency,” including the East-West oil pipeline, relatively prudent fiscal policy, and the accumulation of a large stock of foreign financial assets.

Saudi Economic Outlook Positive If U.S.-Iran Deal Holds

If the memorandum of understanding between the United States and Iran holds, the Saudi economy will grow strongly in the second half of 2026 and into 2027.

The Impact of the Iran War on the Saudi Economy

The U.S.-Israeli war with Iran has led to slower economic growth and disrupted trade in Saudi Arabia, but to date inflation has been unaffected.

Events

Mar 11, 2026

Shockwaves From Iran: Implications for Energy Markets and the Global Economy

On March 11, AGSI hosted a discussion on global energy and economic market volatility.

Speakers

Jan 8, 2026

Outlook 2026: Prospects and Priorities for U.S.-Gulf Relations in the Year Ahead

On January 8, AGSI hosted a virtual roundtable with its leadership and scholars as they look ahead and assess trends likely to shape the Gulf region and U.S. foreign policy during the coming year.

Speakers

Dec 15, 2025

Looking to 2026: Economic Prospects and Policy Challenges in the GCC

On December 15, AGSI hosted a discussion on the future of Gulf economies.

Speakers

Sep 4, 2025

Saudi Arabia: Sustaining Strong Growth Amid Global Economic Uncertainty

On September 4, AGSI hosted a discussion on the International Monetary Fund’s 2025 Article IV report on Saudi Arabia.

Speakers