May 5, 2026

Gulf PMIs Raise Specter of Stagflation

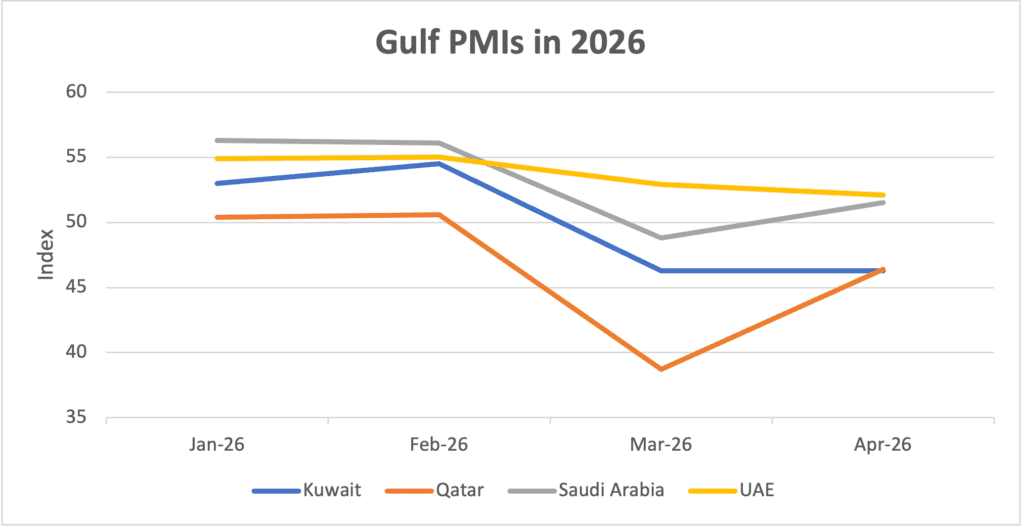

Business conditions in the Gulf generally improved in April, but they remained weaker than before the Iran war. There are signs that price pressures are increasing as the conflict impedes trade.

A purchasing managers’ index is published by S&P Global for Kuwait, Qatar, Saudi Arabia (jointly with Riyadh Bank), and the United Arab Emirates. The PMI is a monthly business survey that asks senior management at companies in the non-oil sector about current and expected future business conditions. The PMI is a useful leading indicator of economic conditions.

In March, PMIs across the Gulf region had fallen, reflecting the impact of the U.S.-Israeli war with Iran. In April, business conditions improved in Kuwait, Qatar, and Saudi Arabia, although the PMIs in Kuwait and Qatar remained below 50, indicating that more companies were still seeing business conditions deteriorate rather than improve. In Saudi Arabia, the PMI moved back above 50 in April (to 51.5 from 48.8 in March), while in the UAE, the PMI weakened slightly further in April to 52.1 (52.9 in March), its weakest level since early 2021.

Source: S&P Global, Riyadh Bank

A feature of the April PMIs for Qatar, Saudi Arabia, and the UAE was the evidence of mounting price and cost pressures in the non-oil sector. The press release for Saudi Arabia noted that “non-oil companies experienced a rapid increase in cost burdens in April as regional instabilities impacted raw material and freight prices. Overall input costs rose at the fastest rate in the survey’s history.” The press release for the UAE commented that, “In order to contain the impact on business margins, average prices charged by firms rose at a historically sharp pace during April. In fact, the rate of inflation was the fastest recorded since June 2011.” For Qatar, it was noted that, “Overall price inflation accelerated sharply to a 16-month high, and was well above the long-run survey average.”

Stagflation Ahead?

The International Monetary Fund’s April 2026 “World Economic Outlook” projected that the Iran conflict would slow global growth and increase inflation, i.e., it would lead to “stagflation.” Although the channels of transmission are different, the April PMIs suggest that stagflation could also be a risk for the Gulf region. For countries outside the Gulf, the main channel through which the conflict affects their economies is the surge in oil prices and the shortages of key oil-related products. For the Gulf, the prices of oil products are still often subsidized, and the main transmission channel is through shipping and air transport disruptions, which make imports costlier.

The path of Gulf economies going forward will be determined by the conflict. Renewed hostilities, which seem a growing risk, would once again hurt business confidence and the growth outlook while putting further upward pressure on prices. A move to a more durable cease-fire, on the other hand, could be expected to underpin a further rebound in confidence and make a recovery in economic activity from the middle of the year more likely. A reopening of established transport routes would also ease price pressures. Last, how governments respond to rising price pressures will also play a role. Increased subsidies or other ways of containing price passthrough to consumers may limit the increase in the official consumer price indices.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

Related

The Iran War and the Saudi Economy

Data shows that the Saudi economy is being negatively affected by the U.S.-Israeli war on Iran, and the impact will likely continue for the next few months at least.

Saudi Economic Spotlight

Apr 2, 2026

Saudi Equities Outperform Global Markets

Saudi equity prices have risen since the start of the Iran conflict, outperforming many regional and global markets. Whether this continues will depend on how and when the conflict ends.

The Saudi Fiscal Deficit in 2025 Was Larger Than Expected

The 2025 budget deficit was larger than expected. The 2026 deficit is also likely to exceed the budget target, but higher oil prices may help contain any overrun.

The Iran War and the Saudi Economy

Data shows that the Saudi economy is being negatively affected by the U.S.-Israeli war on Iran, and the impact will likely continue for the next few months at least.

Apr 2, 2026

Saudi Equities Outperform Global Markets

Saudi equity prices have risen since the start of the Iran conflict, outperforming many regional and global markets. Whether this continues will depend on how and when the conflict ends.

The Saudi Fiscal Deficit in 2025 Was Larger Than Expected

The 2025 budget deficit was larger than expected. The 2026 deficit is also likely to exceed the budget target, but higher oil prices may help contain any overrun.

Analysis

The Trump Presidency, Iran War, and U.S.-Gulf Economic Relationship

The outbreak of the Iran war has halted the deepening of the economic relationship between the United States and the Gulf countries. While likely temporary, it could take some time before the upward trajectory is restored.

Have Saudi Labor Market Reforms Run Their Course?

Recent data suggests that the positive impact of a decade of reforms to improve Saudi labor market outcomes may now be waning.

Saudi Arabia Weathers the Iran War Thanks to Investments in “Economic Resiliency”

The impact of the Iran war on the Saudi economy has been mitigated by investments in “economic resiliency,” including the East-West oil pipeline, relatively prudent fiscal policy, and the accumulation of a large stock of foreign financial assets.

Saudi Economic Outlook Positive If U.S.-Iran Deal Holds

If the memorandum of understanding between the United States and Iran holds, the Saudi economy will grow strongly in the second half of 2026 and into 2027.

Events

Mar 11, 2026

Shockwaves From Iran: Implications for Energy Markets and the Global Economy

On March 11, AGSI hosted a discussion on global energy and economic market volatility.

Speakers

Jan 8, 2026

Outlook 2026: Prospects and Priorities for U.S.-Gulf Relations in the Year Ahead

On January 8, AGSI hosted a virtual roundtable with its leadership and scholars as they look ahead and assess trends likely to shape the Gulf region and U.S. foreign policy during the coming year.

Speakers

Dec 15, 2025

Looking to 2026: Economic Prospects and Policy Challenges in the GCC

On December 15, AGSI hosted a discussion on the future of Gulf economies.

Speakers

Sep 4, 2025

Saudi Arabia: Sustaining Strong Growth Amid Global Economic Uncertainty

On September 4, AGSI hosted a discussion on the International Monetary Fund’s 2025 Article IV report on Saudi Arabia.

Speakers