A United Arab Emirates navy ship sails next to a cargo ship in the Strait of Hormuz as seen from Khor Fakkan, the UAE, March 11. (AP Photo/Altaf Qadri)

The Iran conflict is negatively affecting economic growth in the Gulf region. Oil and gas production is being cut back because of the closure of the Strait of Hormuz. This in turn is having a knock-on effect on industries, such as refining and petrochemicals. Imports for domestic consumption and investment are being disrupted because of the inaccessibility of ports on the Gulf coast. Further, Iranian missile and drone attacks have disrupted travel, transportation, logistics, and technology services, negatively affecting confidence, investment, and tourist arrivals. Some expatriates have also departed, at least temporarily.

The economic impact of the conflict will depend on its length and how it is resolved, both of which remain very uncertain at this stage. A longer conflict will result in larger economic losses although also likely a stronger rebound once the conflict ends. A conclusion to the conflict that leaves in doubt the future security of the region will have implications for the ability to attract investment, talent, and visitors and raises the possibility of longer-term economic “scarring” that the Gulf countries cannot afford given their ambitious growth and diversification agendas.

Impact of Conflict Varies Across Countries

The conflict is affecting all the Gulf countries, but the size of the economic hit varies depending on country characteristics and circumstances. These include the size of the oil and gas production cuts; importance of hydrocarbon production and revenue to the economy; reliance on tourism, logistics, and industries such as petrochemicals; importance of skilled expatriates in the workforce; and extent of the financial buffers that are available to cushion the negative economic fallout.

It seems that Oman and Saudi Arabia are best placed to absorb the impact of the conflict. Their oil exports and broader trade flows are less dependent on passage through the Strait of Hormuz (for Saudi Arabia, because of the East-West pipeline and availability of ports on the Red Sea coast), and their domestic economies are less reliant on foreign labor and investment. Kuwait (which is less reliant on foreign investment) and Qatar have no alternative outlet for their oil and gas given their geographic location, and a large Qatari liquefied natural gas facility is reported to have been badly damaged. In the United Arab Emirates, Abu Dhabi can pipe some of its oil to Fujairah, although this is not without risk given drone attacks on the facility, and Dubai is being significantly affected by the regional risk reassessment that is currently underway by investors, visitors, and employees. Bahrain has an exceptionally weak financial position with government debt already around 140% of gross domestic product, one of the highest in the world. This means that in the absence of financial support from its Gulf neighbors it has no fiscal room to respond to the current situation.

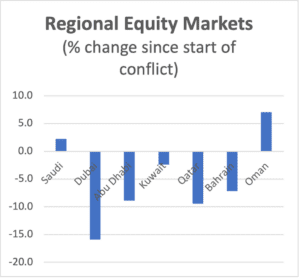

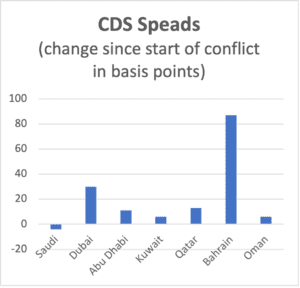

Financial markets and economic forecasters seem to broadly concur with this ranking of relative impact. Equity markets in Oman and Saudi Arabia have risen since the conflict started, and credit default swap spreads, which measure the cost of insuring against the default of a borrower, have changed little. Kuwait has seen a small drop in its equity market and a small rise in credit default swap spreads. Equity markets in Abu Dhabi, Bahrain, and Qatar have fallen by 5% to 10%, while Dubai has been the worst affected experiencing a 15% drop. For comparison, U.S. markets are down about 5% over the same period. Credit default swap spreads have also risen sharply for Bahrain and Dubai.

Source: Country stock exchanges

Source: Marex Emerging Markets Strategy

Forecasts by Goldman Sachs suggest that Oman and Saudi Arabia will be the least impacted by the conflict (declines in real GDP in 2026 of less than 2% and around 5%, respectively), while the other four countries could potentially see declines of 8% to 10%. These forecasts, however, are very dependent on the assumptions made about the length and severity of the conflict.

What’s Next

The Gulf economies will be negatively affected by the conflict, but the extent of the impact is not clear both because of uncertainty about the duration and future intensity of the conflict itself and because there is very little data available at the moment to gauge the initial economic impact of the hostilities. The latter, however, will change in the coming weeks. One of the first useful indicators to be published will be the purchasing managers index for March, which will give a reading of how business sentiment has changed since the conflict started. The index is available for several Gulf countries and will be published in early April. There is little doubt the index will decline in March relative to February, but the size of the drop relative to the start of the coronavirus pandemic will give a useful gauge of the scale of the current disruption to the Gulf economies. The April OPEC “Monthly Oil Market Report,” which will be published mid-month, will also be important to give the first official data on how crude oil production has been affected. Further out, and with varying availability across countries, data on central bank foreign exchange reserves (to see the extent of capital outflows), prices (to see how port closures are affecting import prices), trade, industrial production, government oil revenue, and GDP will be published and gradually clarify the initial economic impact of the conflict. Ultimately, and in line with the experience during the coronavirus pandemic, initial economic forecasts will evolve considerably as this new information is published.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

The early reactions of regional stock markets reflect serious concerns but not full-blown panic despite an unprecedented escalation of the Iran conflict.

The longer the conflict lasts, and the more damage to energy facilities, the greater the risk of oil market tightness, rising prices, and stranded commodities.

If the memorandum of understanding between the United States and Iran holds, the Saudi economy will grow strongly in the second half of 2026 and into 2027.

The Saudi budget recorded a large deficit in the first quarter of 2026 as spending surged, but higher oil revenue during the rest of the year should limit the size of the annual fiscal deficit.

Business conditions in the Gulf generally improved in April, but they remained weaker than before the Iran war. There are signs that price pressures are increasing as the conflict impedes trade.

On January 8, AGSI hosted a virtual roundtable with its leadership and scholars as they look ahead and assess trends likely to shape the Gulf region and U.S. foreign policy during the coming year.