A tugboat assists a cargo ship to dock at the Dammam Port in Dammam, Saudi Arabia, May 17. (REUTERS/Mohammed Benmansour)

The impact that the U.S.-Israeli war with Iran is having on the Saudi economy is becoming clearer as more economic data is released by the statistical authority and other providers. The data shows slowing growth and a big dislocation in trade but a limited impact on inflation. The Saudi equity market has given up the gains it made earlier in the conflict.

Economic Impact of the Conflict – An Update

The impact of the conflict can be seen in trade, growth, inflation, and financial market data.

Trade

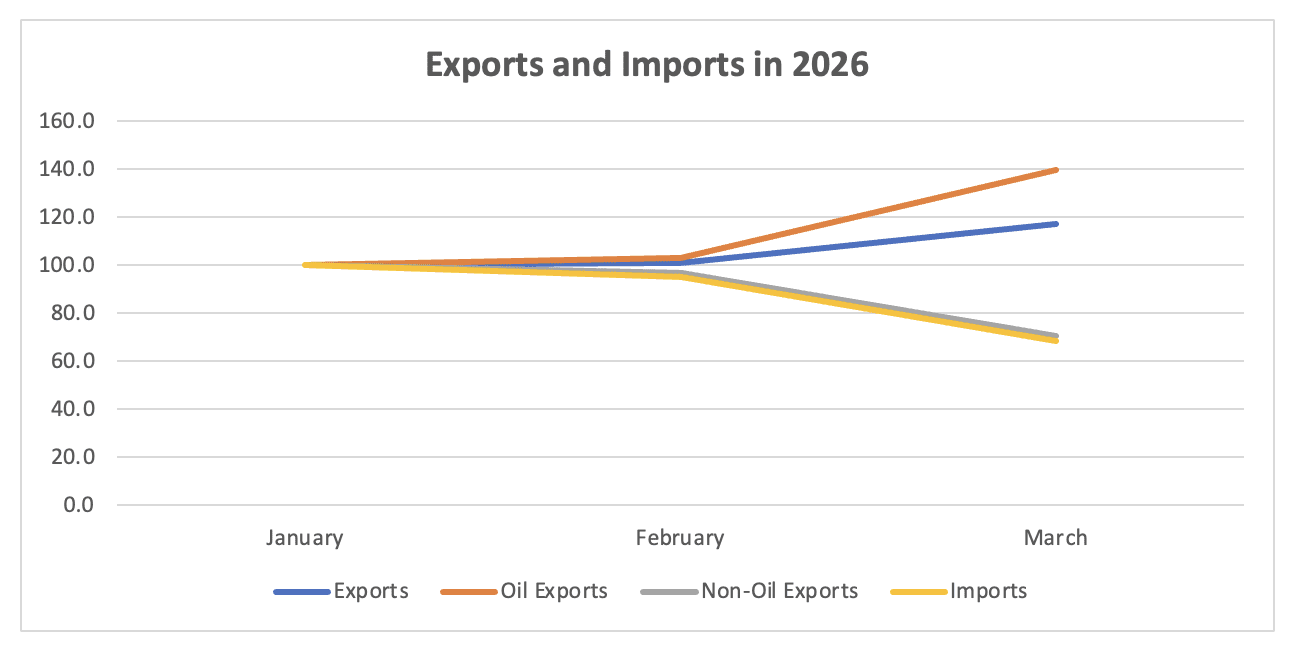

There was a significant improvement in the Saudi trade balance in March relative to February as the value of exports increased by 16%, and the value of imports fell by 28%. The volume of both exports and imports dropped as the Iran conflict disrupted trade through the Strait of Hormuz, but while oil prices rose sharply, offsetting the drop in export volumes, import (and non-oil export) prices remained broadly unchanged.

Sources: General Authority for Statistics; author calculations Note: Numbers in riyals are converted into an index where January 2026 = 100

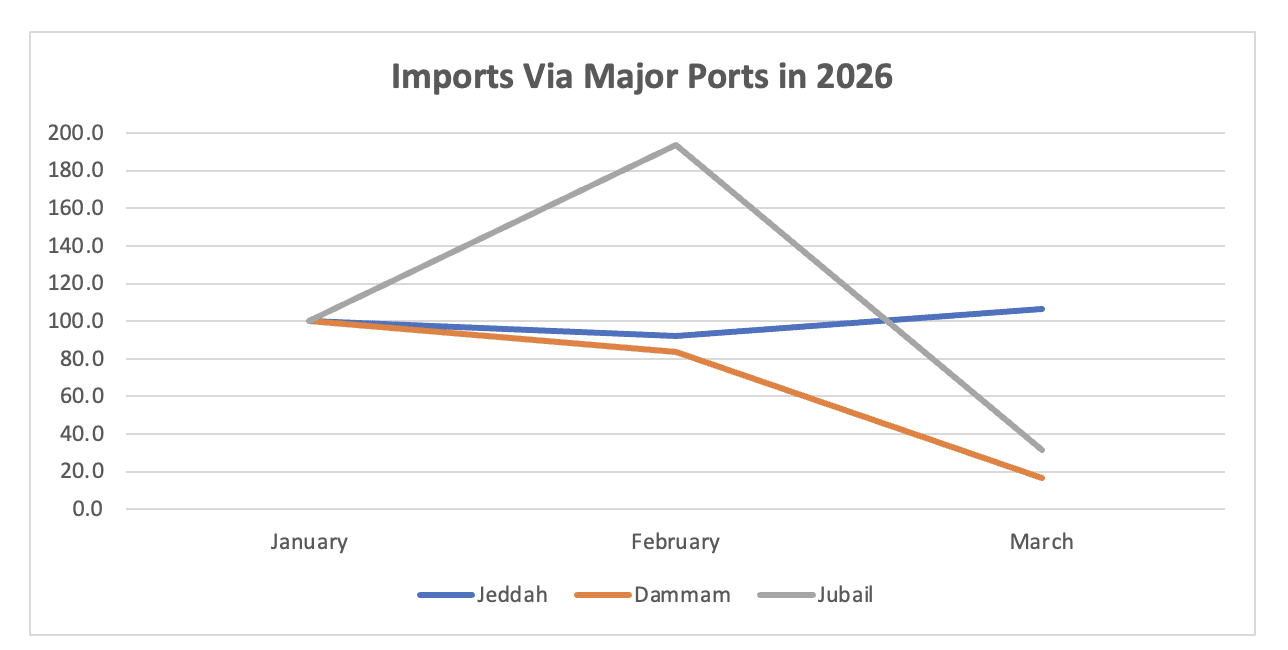

The value of oil exports jumped 36% in March compared to February, as higher oil prices more than offset lower volumes. The number of barrels of crude oil exported fell to 5 million barrels per day, a 32% decline from February, while exports of oil products fell to 1.1 mb/d (down 30% from February). Non-oil exports declined by 27% driven by sharp declines in petrochemical and metal exports with big drops in cargos transiting through the Jubail and Dammam ports. The decline in imports in March was broad based, although particularly large in the machinery/electrical and transport equipment categories. The decline in imports through the Dammam and Jubail ports was only slightly offset by increased traffic through Jeddah port.

Sources: General Authority for Statistics; author calculations Note: Numbers in riyals are converted into an index where January 2026 = 100

Growth

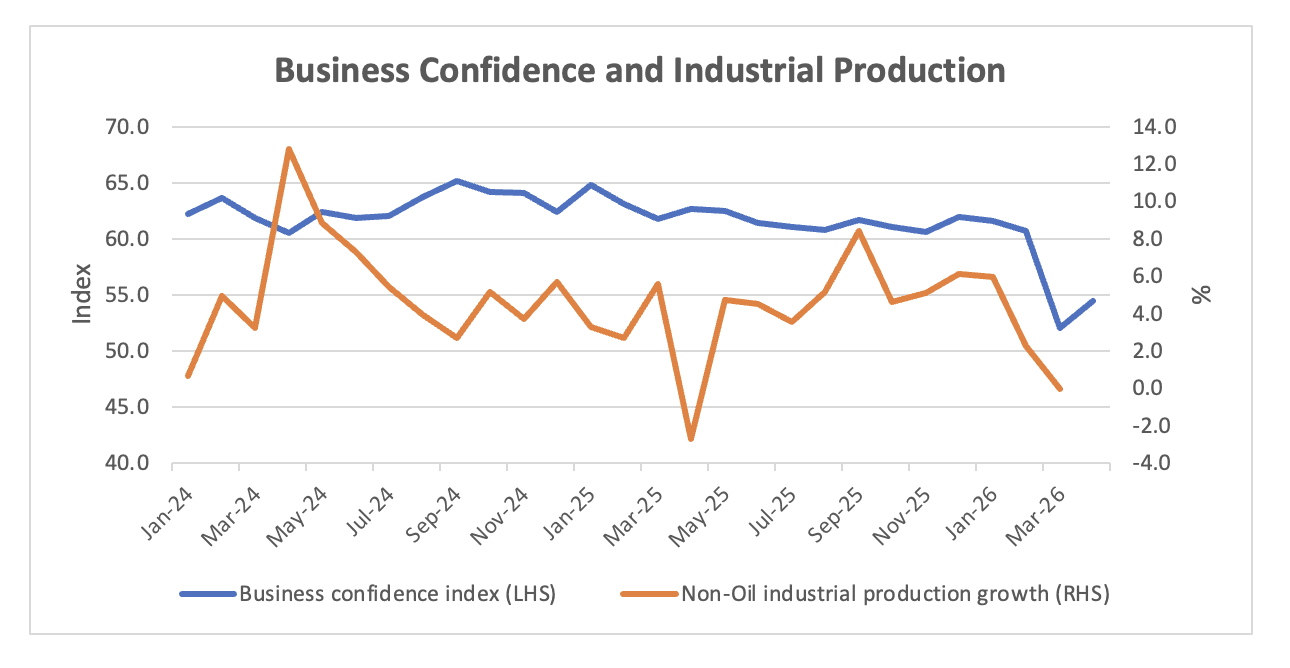

Oil production dropped further to 6.3 million barrels per day in April compared to 7 mb/d in March and 10.9 mb/d in February (OPEC data). In the non-oil sector, industrial output growth slowed to near zero (year on year) in March from 6% as recently as January. The petrochemical sector was the main reason, with production declining by 4.5% year on year. Business confidence in April, however, partially rebounded from its slump in March. Both the purchasing managers’ index published by Riyadh Bank and the business confidence index released by the statistical authority were above 50 in April, indicating that more companies reported that business conditions were improving than deteriorating during the month.

Source: General Authority for Statistics

Inflation

The April purchasing managers’ index raised concerns about rising price pressures on businesses, but there is no evidence to date in the official inflation data that the war is pushing up prices. Annual consumer price inflation remained at 1.7% in April, unchanged from its prewar rate. The key driver of inflation remains housing rents, which increased by 4.5% in April. Food and household energy costs, two areas where other countries are experiencing price pressures, saw price increases of less than 1% year on year in April. For comparison, consumer price index inflation in the United States was 3.8% in April compared to 2.4% in February with the increase driven by higher energy (up 18%) and to a lesser extent food (up 3.2%) prices.

Equity Market

The Saudi equity market is currently up by 3% from its preconflict level, but it has backed off the highs it reached in mid-April. Aramco’s share price continues to perform well, rising by close to 12% since late February, but other sectors have struggled, as the effects of the war have become more apparent. For comparison, the S&P 500 index in the United States is up by 8% since the conflict started.

Assessing the Outlook

The continuing uncertainty about how the Iran conflict will evolve and its eventual outcome makes it very difficult to have confidence in economic forecasts. The data discussed above, however, begins to give a picture of how the Saudi economy is being affected by the conflict. It is increasingly clear that there will be a very large decline in real gross domestic product in the second quarter of 2026 (perhaps as large as 10% year on year), driven by the decline in oil output but reinforced by a smaller contraction in the non-oil economy. Nevertheless, provided that there is no resumption of large-scale military hostilities and that a gradual reopening of the Strait of Hormuz takes place in the second half of the year, there should be a strong rebound in the economy from the third quarter. For the year as a whole, real GDP is likely to contract by around 1% based on real oil GDP falling by 7.5% and real non-oil GDP growing by 2% to 2.5%. Inflation is likely to remain subdued both because of the caps introduced on rent increases in 2025 and because basic food items and energy costs will be subsidized by the government to prevent pass-through to households. Trade flows will adjust as imports and non-oil exports continue to relocate toward Red Sea ports, although the extent of the available capacity at these ports is unclear, and it is unlikely that they can fully compensate for the loss of trade through the Strait of Hormuz.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

Billions of dollars in infrastructure destruction from the war, combined with decades of mismanagement, corruption, and international sanctions, has sparked an unprecedented economic crisis in Iran.

If the memorandum of understanding between the United States and Iran holds, the Saudi economy will grow strongly in the second half of 2026 and into 2027.

The Saudi budget recorded a large deficit in the first quarter of 2026 as spending surged, but higher oil revenue during the rest of the year should limit the size of the annual fiscal deficit.

Business conditions in the Gulf generally improved in April, but they remained weaker than before the Iran war. There are signs that price pressures are increasing as the conflict impedes trade.

Data shows that the Saudi economy is being negatively affected by the U.S.-Israeli war on Iran, and the impact will likely continue for the next few months at least.

On January 8, AGSI hosted a virtual roundtable with its leadership and scholars as they look ahead and assess trends likely to shape the Gulf region and U.S. foreign policy during the coming year.