Saudi Arabia Weathers the Iran War Thanks to Investments in “Economic Resiliency”

The impact of the Iran war on the Saudi economy has been mitigated by investments in “economic resiliency,” including the East-West oil pipeline, relatively prudent fiscal policy, and the accumulation of a large stock of foreign financial assets.

A drone view shows Riyadh, Saudi Arabia, June 1, 2025. (REUTERS/Mohammed Benmansour)

For a country that has been directly in the firing line of the U.S.-Israeli war with Iran, the Saudi economy has held up quite well. Yes, economic growth has slowed, but inflation has remained contained, modest employment growth has continued, and the unemployment rate has declined. The relatively limited economic impact can be attributed to several key pillars of the country’s long-term oil and economic policy strategy. Saudi Arabia has built redundancies and buffers into its strategy to help it manage worst-case scenarios, such as the war. In other words, the country has invested in “economic resiliency.” Three areas are particularly important to support this resiliency:

Aramco has built resiliency into its oil strategy. It has built spare oil production capacity (the International Energy Agency estimates that sustainable production capacity is around 12 million barrels per day compared to actual production before the war of 10.3 mb/d), has invested in considerable oil storage capacity at home and abroad, and has constructed over several decades the East-West oil pipeline to the Red Sea port of Yanbu. This pipeline has been essential in ensuring oil exports continued (albeit at a lower level) while the Strait of Hormuz was closed.

The government has maintained a relatively strong and resilient fiscal position. Low public debt means the government can borrow and spend to support the economy during times of uncertainty, compensating for any pullback in private demand. This flexibility was apparent in the first quarter of 2026 when government spending increased sharply.

Saudi Arabia has a large stock of foreign financial assets ($1.6 trillion) that provides an important buffer against unexpected developments. These assets can be sold to provide foreign currency liquidity and prevent depreciation pressures developing on the exchange rate.

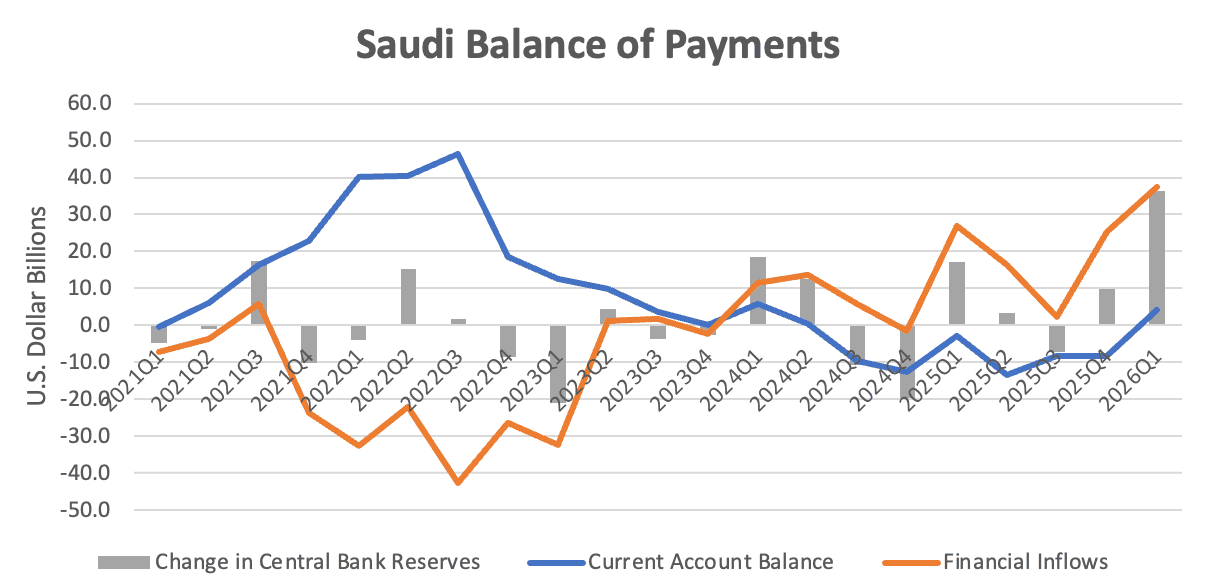

Current Account Into Surplus, Central Bank Reserves Increase

The recently released balance of payments data for the first quarter of 2026 provides further evidence of the resilience of the Saudi economy. The current account moved into a surplus of $4.1 billion, the first surplus for nearly two years, from a deficit of $8.2 billion in the fourth quarter of 2025. The move into surplus was due to:

An increase in the trade surplus as oil export revenue rose (higher prices more than offsetting lower export volumes), and imports fell due to shipping disruptions in the Strait of Hormuz. Non-oil export revenue also fell.

A narrowing of the deficit on the services account, driven by an improved travel balance. Spending by foreigners visiting Saudi Arabia increased while spending by Saudis traveling overseas declined relative to the fourth quarter of 2025.

These two factors were only partly offset by an increase in remittance outflows from expatriates working in Saudi Arabia.

At the same time, there were large financial inflows into Saudi Arabia in the first quarter of 2026 as:

Saudis sold close to $23 billion of foreign equity and investment funds, the largest quarterly sale on record. The proceeds of these sales were partly repatriated but were also used to increase deposits held with foreign financial institutions (by $15 billion), indicating the desire to increase foreign currency liquidity in the face of the uncertainty from the war. It is likely that these sales were driven by public entities such as the public pension fund and the Public Investment Fund, although there is no data to confirm this.

Saudi residents borrowed $27 billion from nonresidents. The government led the way, borrowing $13 billion, although much of this borrowing took place before the war started. Borrowing is typically heavy in the first quarter of the year, as the government usually moves early to meet its annual borrowing need.

Foreign investors did not repatriate funds to any significant degree. In aggregate, foreign investors were net purchasers of Saudi equities in the first quarter following the liberalization of rules around foreign ownership despite some modest selling in the early days of the conflict.

Source: Saudi Central Bank Note: Financial inflows are defined as the sum of direct investment, portfolio, and “other inflows.” A positive number is an inflow into Saudi Arabia.

As a result of the current account surplus and the financial inflows, net foreign assets held by the Saudi Central Bank increased by $36 billion in the first quarter to around $500 billion. This provides a very large financial cushion to protect the pegged exchange rate (to the U.S. dollar) during times of economic pressure. The increase in foreign assets in the early part of this year could be considered surprising – a country directly affected by a negative event, such as the Iran war, would usually see its central bank reserves (and exchange rate) come under pressure as domestic and foreign investors move capital out of the country. This didn’t happen for Saudi Arabia because oil revenue increased, foreign assets were sold and borrowing increased, and foreigners remained invested in the local equity market.

Resilience Will Remain a Key Focus of Saudi Policymakers

The war has reiterated the importance of economic resilience and effective contingency planning. Without the far-sighted investment in the East-West oil pipeline and the long-established policies of limiting government debt and maintaining a large stock of relatively liquid foreign assets, the impact of the war on the Saudi economy would have been larger.

In the coming years, Saudi policymakers are likely to continue to make investments in economic resiliency. These could include the further development of the Red Sea ports, new and expanded oil pipelines, and better air, rail, and road infrastructure in the country and across the broader region. Many of these investments will provide benefits in “normal” times as well as providing added resilience in case of future disruptions.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

If the memorandum of understanding between the United States and Iran holds, the Saudi economy will grow strongly in the second half of 2026 and into 2027.

If the memorandum of understanding between the United States and Iran holds, the Saudi economy will grow strongly in the second half of 2026 and into 2027.

The Saudi budget recorded a large deficit in the first quarter of 2026 as spending surged, but higher oil revenue during the rest of the year should limit the size of the annual fiscal deficit.

Business conditions in the Gulf generally improved in April, but they remained weaker than before the Iran war. There are signs that price pressures are increasing as the conflict impedes trade.

On January 8, AGSI hosted a virtual roundtable with its leadership and scholars as they look ahead and assess trends likely to shape the Gulf region and U.S. foreign policy during the coming year.