Apr 2, 2026

Saudi Equities Outperform Global Markets

Saudi equity prices have risen since the start of the Iran conflict, outperforming many regional and global markets. Whether this continues will depend on how and when the conflict ends.

As the U.S.-Israeli conflict with Iran moves into its second month, the Gulf continues to face drone and missile attacks, the destruction of infrastructure and property, the curtailment of oil and gas exports, and uncertainty about how and when the conflict will end.

Through these challenges, however, the Saudi equity market has proved to be remarkably resilient. After dropping during the first few days of the conflict, the Tadawul All Share Index has recovered and is now up by 5% since the start of hostilities. This stands in contrast to most other regional and global markets. U.S. equity prices are down by around 5%, the Dubai market by 15%, and an index of world equity prices has declined by around 6%.

Why Have Saudi Equity Prices Risen During the Conflict?

At least three factors have supported the Saudi equity market. First, despite the closure of the Strait of Hormuz, Saudi Arabia can export a significant amount of oil and oil products via Yanbu on the west coast with the East-West oil pipeline now reported to be operating at its full capacity of 7 million barrels per day. Reflecting this, Aramco’s share price has risen by 10% since the start of the conflict as investors bet that higher oil prices will offset lower oil export volumes and support Aramco’s earnings. Given its high weight (around 15%) in the Tadawul index, Aramco’s rising share price has given the overall market a boost.

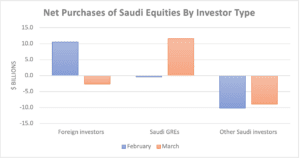

Source: Tadawul; author calculations

Second, the market has been supported by equity purchases by government-related enterprises (specific institutions involved are not disclosed). These have offset sales by Saudi individual investors and to a lesser extent by foreign investors. Sales by the latter followed the surge in their purchases in February after restrictions on foreign investor participation in the Saudi markets were eased.

Third, the Saudi economy is in a better position than most of its Gulf neighbors’ because of its larger size, lower exposure to the Strait of Hormuz, and less dependence on foreign capital and skilled labor. This should mean it experiences a smaller hit to economic growth than other countries in the region.

What’s Next?

Global oil and financial markets continue to swing wildly from day to day as investors react to President Donald J. Trump’s latest words and social media posts about the likely duration and endgame of the conflict.

Against this uncertainty, can the Saudi market stay in positive territory? A quick end to the conflict with the reopening of the Strait of Hormuz would almost certainly boost Saudi equity prices, particularly if full oil production is restored quickly and the oil price settles above its pre-conflict level as seems likely (financial markets are currently pricing Brent crude for December 2026 delivery at $78 per barrel compared to $69/bbl pre-conflict). In turn, this would help industries, such as petrochemicals, that are being forced to cut production and minimize the risks of longer-term damage to investor and foreign visitor confidence.

A longer conflict or one that ends with Gulf security issues unresolved, however, would make it much harder for equity prices to stay in positive territory, as the damage to economic growth would be greater. A particularly negative scenario would be the resumption of attacks on ships navigating the Bab el-Mandeb strait, which would disrupt oil shipments to Asia.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

Related

The Saudi Fiscal Deficit in 2025 Was Larger Than Expected

The 2025 budget deficit was larger than expected. The 2026 deficit is also likely to exceed the budget target, but higher oil prices may help contain any overrun.

Putting the 2026 Saudi Budget Under the Microscope

The Saudi government projects that the budget deficit will narrow during 2026-28, but this will depend on a rebound in oil prices and tight control of spending.

Saudi Economic Spotlight

Nov 19, 2025

The Saudi Trade and Investment Commitment to the United States in Perspective

The $1 trillion Saudi trade and investment commitment to the United States will be extremely difficult to achieve given the size of the Saudi economy and its current financial situation.

The Saudi Fiscal Deficit in 2025 Was Larger Than Expected

The 2025 budget deficit was larger than expected. The 2026 deficit is also likely to exceed the budget target, but higher oil prices may help contain any overrun.

Putting the 2026 Saudi Budget Under the Microscope

The Saudi government projects that the budget deficit will narrow during 2026-28, but this will depend on a rebound in oil prices and tight control of spending.

Nov 19, 2025

The Saudi Trade and Investment Commitment to the United States in Perspective

The $1 trillion Saudi trade and investment commitment to the United States will be extremely difficult to achieve given the size of the Saudi economy and its current financial situation.

Analysis

Saudi Economic Outlook Positive If U.S.-Iran Deal Holds

If the memorandum of understanding between the United States and Iran holds, the Saudi economy will grow strongly in the second half of 2026 and into 2027.

The Impact of the Iran War on the Saudi Economy

The U.S.-Israeli war with Iran has led to slower economic growth and disrupted trade in Saudi Arabia, but to date inflation has been unaffected.

May 6, 2026

Spending Surge Puts Saudi Budget in Large First Quarter Deficit

The Saudi budget recorded a large deficit in the first quarter of 2026 as spending surged, but higher oil revenue during the rest of the year should limit the size of the annual fiscal deficit.

May 5, 2026

Gulf PMIs Raise Specter of Stagflation

Business conditions in the Gulf generally improved in April, but they remained weaker than before the Iran war. There are signs that price pressures are increasing as the conflict impedes trade.

Events

Mar 11, 2026

Shockwaves From Iran: Implications for Energy Markets and the Global Economy

On March 11, AGSI hosted a discussion on global energy and economic market volatility.

Speakers

Jan 8, 2026

Outlook 2026: Prospects and Priorities for U.S.-Gulf Relations in the Year Ahead

On January 8, AGSI hosted a virtual roundtable with its leadership and scholars as they look ahead and assess trends likely to shape the Gulf region and U.S. foreign policy during the coming year.

Speakers

Dec 15, 2025

Looking to 2026: Economic Prospects and Policy Challenges in the GCC

On December 15, AGSI hosted a discussion on the future of Gulf economies.

Speakers

Sep 4, 2025

Saudi Arabia: Sustaining Strong Growth Amid Global Economic Uncertainty

On September 4, AGSI hosted a discussion on the International Monetary Fund’s 2025 Article IV report on Saudi Arabia.

Speakers