Israel-Iran Conflict Reveals Resilience and Vulnerability of GCC Economies

The latest regional conflict reinforced how difficult it is to severely disrupt economic momentum in the Gulf Cooperation Council while highlighting genuine threats to economic security and public safety in the region.

Delegates visit Saudi Arabia's pavilion during the Arabian Travel Market exhibition in Dubai, United Arab Emirates, April 29. (AP Photo/Altaf Qadri)

The fragile cease-fire between Israel and Iran ended – for now – a worrying period of regional conflict. Gulf Cooperation Council countries’ economies proved resilient amid the recent flare up of the Israel-Iran conflict. In the initial days following the cease-fire, Gulf economic indicators and forecasts looked relatively upbeat, though certain industries suffered short-term disruptions. Similar demonstrations of economic resilience occurred during past clashes and regional conflicts.

This latest conflict nevertheless posed a significant stress test for Gulf countries caught in the middle of the escalation. Israel targeted Iranian nuclear facilities and scientists, and both sides openly attacked their rival’s energy infrastructure. The United States entered the conflict by dropping bunker-busting bombs on Iranian nuclear facilities. President Donald J. Trump announced that these U.S. attacks “totally obliterated” Iran’s key nuclear enrichment facilities, but other preliminary intelligence assessments suggested a more limited degrading of the core components of Iran’s nuclear program.

Iran also targeted the U.S. Al Udeid Air Base in Qatar. There were indications that it was a symbolic and choreographed attack, which minimized damage. But the attack nevertheless marked a spillover of the conflict to a GCC member country that is among the least hawkish on Iran.

The 12-day conflict therefore presented a mixed bag for GCC economies. Having emerged largely unscathed, Gulf governments can manage the short-term disruptions and proceed with their ambitious economic development agendas. Yet the evolving nature of this conflict – direct and open targeting of regional energy infrastructure, nuclear facilities, and a U.S. base in a GCC country – could impose challenges around building business and investor confidence over the medium and longer terms, if such conditions recur.

Limited Short-Term Impact

Gulf stock markets dipped initially but quickly rebounded, despite news of U.S. strikes on Iranian nuclear facilities. Regional stock markets extended gains following news of the cease-fire. On June 26, Dubai’s benchmark stock index reached a 17-year high.

Gulf airlines had to suspend flights and alter routes, and Qatar temporarily closed its airspace on June 23 to ensure the safety of citizens, residents, and visitors. The return to normal flight and cargo schedules will be welcomed in the region, given the sector’s importance to regional economies. The aviation sector supported 27% of Dubai’s gross domestic product in 2023. And Gulf airlines achieved significant gains amid stock market rallies in the region following the cease-fire announcement.

The conflict is likely to dent tourism flows over the immediate term, as potential visitors wait to see whether the conflict flares up again. There may well be tourists who opt to avoid the region altogether out of security concerns, but this dynamic is unlikely to significantly impact overall figures for the sector, absent new conflict escalations.

The broader Middle East and North Africa region’s tourism sector has proved resilient in recent years, leading global tourism growth in the first three quarters of 2024 despite major conflicts, according to the World Bank. From October 2023-24, GCC countries posted positive growth in aviation passenger arrivals. Like aviation, tourism is a key sector for the region. The travel and tourism sector accounted for 13% of the United Arab Emirates’ GDP in 2024.

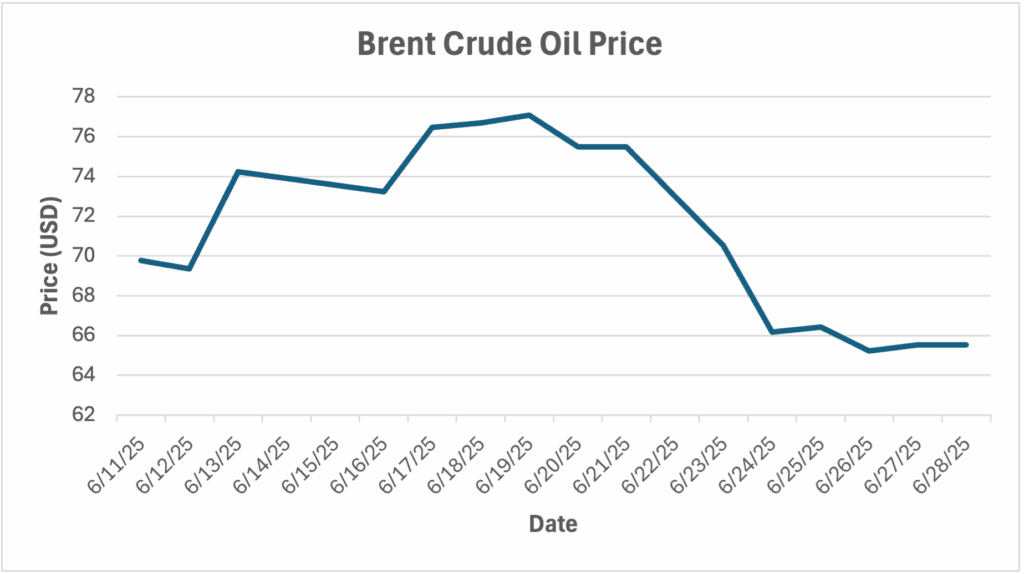

The conflict did not result in major and enduring shifts in the oil price environment, which directly impact the fiscal position of Gulf governments. Brent crude oil prices jumped from $69.36 per barrel on June 12 to $74.23/bbl on June 13, after Israel began launching strikes on Iran. Brent crude prices peaked at $77.08/bbl on June 19 before dropping steeply over the subsequent days and hovering around $66/bbl during the last week of June. Brent crude oil rested between $60/bbl and $70/bbl for most of April, all of May, and the early part of June. This price point reflects neither an economic crisis nor financial windfall for regional governments.

Source: Oilprice.com

Goldman Sachs estimated a $10 geopolitical risk premium on Brent crude as long as there are no major disruptions to energy production and exports in the region, though that premium assessment dropped in the aftermath of the cease-fire. Gulf government officials do not want to see rising geopolitical tensions and war in their neighborhood. However, they won’t mind bringing more oil to market at elevated prices, especially with an unwinding of OPEC+ oil production curbs underway. OPEC+ is likely to proceed with another “accelerated three-month phase-in of barrels,” beginning in August.

GCC economies are expected to grow at a healthy pace in 2025 – in large part because of higher oil production. A recent report by the Institute of Chartered Accountants in England and Wales and Oxford Economics revised upward their estimate for the GCC’s GDP growth this year to 4.4% from 4% with Saudi Arabia and the UAE expected to lead regional growth. On June 25, Fitch Ratings affirmed its AA- rating for the UAE alongside an expectation that the conflict with Iran will “remain contained and short-lived.”

Greater Longer-Term Uncertainty

Perceptions that the Gulf is an increasingly dangerous and unstable neighborhood pose a potential economic headwind, though a difficult one to measure. This conflict – like those preceding it – threatens to project risk by association and proximity. Nearly two weeks of constant news coverage of missile and drone attacks does not make for compelling commercial marketing and investment promotion material. Nor are concerns over radiation exposure and reports of a collective framework to monitor potential radiation encouraging developments for Gulf citizens and residents. Governments in countries where foreigners constitute a significant majority of the population, such as the UAE and Qatar, are perpetually concerned about shocks that could initiate an exodus of residents, though such a scenario has not materialized, and there remain strong financial incentives keeping expatriates in place as long as possible.

Iran-aligned proxies, and likely Iran itself, have attacked Gulf critical infrastructure in recent years. But the direct Iranian attack on a U.S. base in Qatar was alarming. Gulf countries may increasingly find themselves in the direct – rather than just indirect – line of fire during future flare ups. A debilitating strike on a major energy facility in the Gulf or the unlikely event of a major obstruction of the Strait of Hormuz would rattle regional governments’ economic security. Multinationals and investors would likewise fret about the fiscal health of governments and government-related entities. Damaging attacks on other critical infrastructure – from airports to desalination plants – would impact a range of economic sectors. That is not to say any of this must happen, but it is possible.

Moving forward, Gulf governments may need to increase incentives for attracting foreign investors, high net worth individuals, skilled professionals, and other long-term residents. If a lower oil price environment continues for some time, as some short-term energy outlooks suggest, then enhancing incentives could be an increasingly bitter pill to swallow, especially as regional governments grapple simultaneously with global macroeconomic uncertainty. Sweetening the commercial incentive pot will be easier for the UAE than Saudi Arabia: Emirati officials oversee a smaller population of citizens and strong fiscal position. Multinational firms operating in specific industries and certain demographic segments of residents and visitors may be easier to attract, given varying degrees of risk tolerance.

Gulf governments will seek to demonstrate that robust diplomatic activity and defenses can permit their countries to remain islands of stability, safety, and wealth in a tumultuous region. Most investors, citizens, and residents understand the regional risks. So, it will be back to business as usual for many. But no one wants the major risks associated with this recent conflict to come knocking on their doors.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

AGSI explains what Israel’s sudden and massive attack on Iran is likely to mean for Gulf Arab states, Iran, the United States, and global and regional economies.

A flurry of economic announcements and initiatives by the Omani government indicate a strong desire to sustain both reform progress and economic momentum amid potential headwinds.

U.S. authorizations for exporting advanced chips to the leading Gulf technology firms is sure to please regional authorities, who will push to broaden and accelerate technology collaboration with the United States.

When the Saudi crown prince meets President Trump in Washington, the main topics of discussion are likely to be commercial deals, a defense pact, a Saudi civilian nuclear program, and normalization with Israel.