Smoke rises above Riyadh, Saudi Arabia, March 5. (REUTERS/Stringer)

A purchasing managers’ index is published by S&P Global for Kuwait, Qatar, Saudi Arabia (jointly with Riyadh Bank), and the United Arab Emirates. The PMI is a monthly business survey that asks senior management at companies in the non-oil sector about current and expected future business conditions. The survey includes questions about output, exports, capacity utilization, inventories, prices, and employment. It asks each survey respondent if business conditions in each of these categories have improved, deteriorated, or stayed the same compared to the previous month. An aggregate PMI is constructed as a weighted average of responses across the various subcategories. The index ranges from 0 to 100 with a reading of 50 indicating that companies saw no change in business conditions compared to the previous month. A reading above 50 indicates that business conditions are improving and a reading below 50 that they are deteriorating.

Deterioration in Business Conditions

The March PMIs are the first to reflect the impact of the U.S.-Israeli war with Iran on business conditions in the Gulf. The surveys were conducted in the second half of March and therefore gave companies time to digest the impact of the conflict on their business. Unsurprisingly, the PMI fell in all four Gulf countries in March although with variation across countries.

The decline in the PMI for Qatar was particularly sharp. The index fell to 38.7 in March from 50.6 in February, taking it close to its record low in May 2020. The press release noted that “New business declined at the fastest rate since the survey began in 2017 as clients delayed spending decisions and new projects, leading to the steepest decline in output since 2020 and survey-record pessimism regarding the outlook.”

Kuwait and Saudi Arabia also saw their PMIs fall below 50, to 46.3 and 48.8 respectively – their lowest levels since 2022 and 2020. For Kuwait, the press release noted that “Reports from companies signalled that the suspension of flights and shipping were key factors leading to renewed reductions in output and new orders, with companies responding to lower workloads by scaling back employment, purchasing activity and inventory holdings.”

Although they declined, the UAE and Dubai-specific PMIs both stayed above 50. These readings are surprising and seem hard to reconcile with reports that the travel and tourism sectors in Dubai have been particularly hard hit. The press release noted that “The UAE non-oil private sector was knocked back by the impacts of the war in the Middle East in March. That said, for many firms, orders books were resilient and output expanded. Anecdotal comments suggested that sectors such as tourism, retail and logistics were the most affected, whereas segments such as technology and construction signalled a softer, but still notable impact.”

Implications for the Saudi Economy

The press release for Saudi Arabia’s March PMI summed up the survey results. It noted that “Responses from non-oil firms highlighted that a steep fall in new export orders and weaker domestic customer confidence had dampened sales and led businesses to reduce their output. Supply chains were also impacted as firms commented on freight delays and rising transport costs, which contributed to a robust rise in backlogs of work. Nevertheless, the impact on price pressures across the sector was subdued, with input costs rising at the softest pace in a year amid weak demand.”

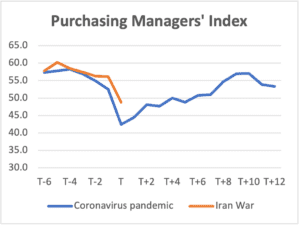

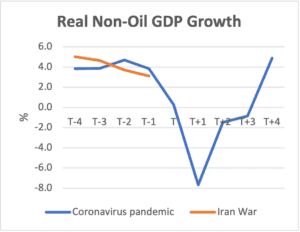

The PMI has proved to be a useful leading indicator for real non-oil gross domestic product in Saudi Arabia, tracking quite closely the turning points in economic growth since it was first published in August 2009. For present purposes, it is useful to compare the PMI now to that during the first months of the coronavirus pandemic in 2020. This is done in the figures below, which for ease of comparison standardize the timeline so that time T is the month (quarter) the event started (March/Q1 2020 for the coronavirus pandemic and March/Q1 2026 for the Iran war). Then T-1, T+1 is the month/quarter before/after the event, etc.

Source: Riyadh Bank; author calculations Note: T is the month of the shock. For the coronavirus pandemic, T is March 2020. For the Iran war, T is March 2026.

Source: General Authority for Statistics; author calculations Note: T is the quarter of the shock. For the coronavirus pandemic, T is 2020Q1. For the Iran war, T is 2026Q1.

In March 2020 (month T), the PMI dropped by 10 points to a record low of 42.4 before it began a gradual and uneven recovery to its prepandemic level by November 2020 (month T+8). This drop in the PMI foreshadowed an economic downturn. Real non-oil GDP growth slowed in the first quarter of 2020 (quarter T), but the biggest impact was in the second quarter (T+1), when the non-oil economy contracted sharply. This delayed impact in the data was because the shock happened toward the end of the first quarter, and so only March was affected, while all three months of the second quarters were affected.

The 8-point drop in the PMI in March 2026 (month T) was the second largest on record. The size of the decline indicates that non-oil sector growth is likely to slow in the first quarter (as in 2020, only one month of the first quarter was affected), and then contract in the second quarter, unless hostilities end very soon and business confidence recovers quickly. The PMI in March 2026, however, remains well above its 2020 low, so the downturn is likely to be shallower than in 2020.

The Outlook

The short-term economic outlook in Saudi Arabia and the broader Gulf region remains closely tied to the length and intensity of the hostilities. While a swift end that provides clarity about the future security of the Gulf countries could see business conditions recover quickly (although infrastructure that has been damaged will take longer to repair), a longer and more intense conflict will likely further erode business sentiment with negative implications for economic activity. As well as damaging non-oil growth prospects, the curtailment of oil and gas exports has seen real hydrocarbon sector output plummet across the Gulf. The extent of this decline will be revealed in the upcoming OPEC and International Energy Agency monthly oil market reports for April.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

The early reactions of regional stock markets reflect serious concerns but not full-blown panic despite an unprecedented escalation of the Iran conflict.

Saudi equity prices have risen since the start of the Iran conflict, outperforming many regional and global markets. Whether this continues will depend on how and when the conflict ends.

The conflict with Iran has curtailed the supply of oil from the Gulf, pushing up the price of the medium and heavier grades it usually exports relative to lighter grades.

With young Saudis continuing to enter their working age years in large numbers, robust employment gains need to continue, but slower non-oil growth may present a challenge.

On January 8, AGSI hosted a virtual roundtable with its leadership and scholars as they look ahead and assess trends likely to shape the Gulf region and U.S. foreign policy during the coming year.