The Luojiashan tanker sits anchored in Muscat, as Iran vows to close the Strait of Hormuz, amid the U.S.-Israeli conflict with Iran, in Muscat, Oman, March 7. (REUTERS/Benoit Tessier)

Crude oil prices surged to $119 per barrel when trading opened March 9, the highest level since 2022, reflecting growing fears that some 20% of global oil supply could remain trapped in the Middle East after the effective closure of the Strait of Hormuz.

Prices retreated after G7 finance ministers signaled they were considering releasing strategic oil reserves to calm markets. But the relief was short lived. Oil began climbing again later in the day after the French minister clarified that governments were not yet ready to release emergency stocks, highlighting the uncertainty surrounding the crisis. The Brent futures contract was trading just below $100/bbl in the late London afternoon.

International Energy Agency Executive Director Fatih Birol reportedly called for a coordinated release of emergency oil reserves during an online meeting with G7 ministers, Reuters reported, quoting Japanese Finance Minister Satsuki Katayama. “IEA called for each country to do a coordinated release of oil reserves,” Katayama said. “In response to the current situation … the G7 has agreed to continue closely monitoring developments in the energy market and to take necessary measures to support global energy supply, including the release of oil reserves.”

In a post on its website on the situation in the Middle East, the IEA wrote that: “Global observed oil inventories rose to more than 8.2 billion barrels in 2025, their highest level since 2021. These stocks now provide a welcome cushion against supply disruptions.” IEA member countries also hold more than 1.2 billion barrels of public emergency stocks, and a further 600 million barrels of industry stocks are held under government obligation.

Yet this reassurance by the IEA has not curbed the current volatility in a market that is facing the most dramatic supply disruption in decades.

Although Iran had frequently threatened to shut down the Strait of Hormuz if attacked, this is the first time that it has succeeded in halting flows through the world’s most important oil transit route not by military means but by making the waterway too risky to navigate. Missile strikes, drone attacks, and soaring insurance costs have brought tanker traffic to a near standstill. Around 19 million barrels of oil per day, roughly 20% of global supply, are now stranded behind the chokepoint, unable to reach global markets.

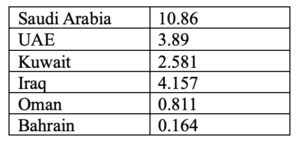

January Oil Production (in mb/d)

Source: OPEC February Monthly Oil Market Report, secondary source estimates (Note: Qatar is not included as it left OPEC in 2018. Its oil production is estimated at around 600,000 b/d)

As the U.S.-Israeli war against Iran enters its second week, the sudden disruption is sending shockwaves through the global energy system, raising fears of a supply shock. Spare production capacity is confined to a handful of Middle Eastern producers unable to get much of that oil to markets.

The price swings reflect the anxiety that has gripped the oil market as the war has dragged on. For the first time in modern history, the Strait of Hormuz – the narrow waterway responsible for roughly 20% of global oil flows – has effectively been closed to commercial shipping. Iranian missile and drone attacks targeting Gulf Arab states have made the passage too dangerous for most tanker operators, bringing traffic to a near standstill.

The closure has left several major oil producers with no viable export routes. Iraq, Kuwait, Qatar, and Bahrain rely almost entirely on Gulf terminals that require tankers to transit the strait. With shipping halted, producers have begun to shut down oil fields as storage tanks fill up and export outlets disappear.

On March 2, Qatar halted all liquefied natural gas production at its Ras Laffan complex, which has nameplate capacity of 77 million metric tons per year, and declared force majeure, after the vast facility was struck by an Iranian drone. The move pushed European gas prices above 60 euros per megawatt hour (approximately $70/MWh), nearly twice as high as before the U.S.-Israeli strikes on Iran began February 28. Although this is still not the gas shock that sent prices to a record high in the wake of Russia’s 2022 invasion of Ukraine, the scramble for spot LNG cargoes is likely to be repeated this time around as Asian and European customers compete for supply in a tight market.

Kuwait Petroleum Corporation has already begun cutting output and declaring force majeure on shipments, while Iraq has moved to shut in major fields for the same reason. Bahrain’s state energy company has also declared force majeure after Iranian strikes set parts of its refinery complex ablaze. Saad Sherida Al Kaabi, Qatar’s minister of energy and CEO of QatarEnergy, warned in a March 6 interview with Financial Times that the crisis in Iran could bring down the world economy. He predicted that other Gulf producers would declare force majeure, which could send prices as high as $150/bbl.

This cascading disruption has effectively wiped out the spare production capacity that the OPEC+ alliance typically relies on to stabilize markets during crises. Saudi Arabia, the United Arab Emirates, Iraq, and Kuwait hold nearly all the world’s spare production capacity, but their exports are currently either blocked or limited.

Even the decision by eight OPEC+ members to accelerate their planned output increases – raising production quotas by a modest 206,000 b/d – has been rendered largely irrelevant. Additional barrels cannot stabilize markets if they cannot be shipped to customers.

The oil shipping industry has been among the first to feel the full force of the crisis. Nearly 250 tankers – around 6% of the global fleet – are now stranded in the Gulf, unable or unwilling to enter the conflict zone. Freight rates have surged as traders scramble to secure vessels for alternative supply routes.

Some shipbrokers have reported that freight costs for very large crude carriers have already reached around $15/bbl, with some unconfirmed fixtures suggesting the possibility of costs rising to $30/bbl. Such levels would represent some of the highest shipping costs seen in modern oil markets.

War-risk insurance premiums have also surged. Ships can still theoretically obtain coverage to sail through the Strait of Hormuz, but policies now cost several times more than before the conflict, further discouraging operators from entering the region.

The disruption has forced importers to seek supply from much further afield, with Atlantic Basin producers increasingly supplying markets that traditionally rely on Middle Eastern crude. These longer shipping routes will tie up vessels for extended periods, further tightening the global tanker fleet.

Against this backdrop, policymakers are considering emergency measures to stabilize markets. G7 ministers are still discussing the possibility of coordinated stock releases, and the initial price reaction March 9 illustrated just how sensitive markets are to that prospect. In parallel, the United States has begun taking smaller steps to ease the pressure. Washington recently issued a 30-day waiver allowing Indian refiners to resume purchases of Russian oil to compensate for the loss of Middle Eastern supply. While this may provide temporary relief, it will not fully offset the disruption of flows through the Strait of Hormuz.

While many Gulf producers are effectively trapped behind the strait, Saudi Arabia and the UAE have contingency plans that allow at least some exports to continue, having invested in infrastructure designed specifically to bypass the Strait of Hormuz during crises. Saudi Arabia’s East-West pipeline carries crude from the kingdom’s eastern oil fields to Yanbu on the Red Sea, while the UAE operates a pipeline that transports Murban crude to the port of Fujairah on the Gulf of Oman. These routes provide the only meaningful outlets for Gulf crude that do not require tankers to pass through the strait.

Saudi Aramco has already begun offering customers the option to load cargoes from Yanbu rather than from Gulf terminals, such as Ras Tanura. Redirecting exports through this route could allow the kingdom to maintain shipments of roughly 2 mb/d, potentially rising toward 3 mb/d if infrastructure is pushed to its limits. Even so, this represents only a fraction of Saudi Arabia’s typical crude exports, which approached 7 mb/d before the conflict.

The UAE’s bypass option is somewhat simpler. Its pipeline to Fujairah can deliver up to 1.8 mb/d of its flagship Murban grade crude to the port, allowing tankers to load outside the Gulf. But this route also faces risks. Iranian drone attacks have already targeted storage facilities at Fujairah, where Abu Dhabi crude continues to load, though volumes are lower than the precrisis level.

A prolonged conflict may well see a further surge in oil prices to levels cited by the Qatari minister, and only the few Gulf exporters with access to the market will benefit. Consumers will pay the price, as higher energy costs feed into other economic sectors and risk dampening global economic growth.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

The early reactions of regional stock markets reflect serious concerns but not full-blown panic despite an unprecedented escalation of the Iran conflict.

There was a growing war risk premium in the oil markets tied to escalating regional tensions; the shift from shadow confrontation to direct military action changes the calculus.

There was a growing war risk premium in the oil markets tied to escalating regional tensions; the shift from shadow confrontation to direct military action changes the calculus.

From the Gulf to the eastern Mediterranean and North Africa, governments are recalibrating fiscal terms, monetization strategies, and partnership models to attract international players.

A founding member of OPEC is now effectively under external control, raising questions about sovereignty, influence, and the resilience of producer-led market management.

The International Energy Agency sees demand increasing as rising living standards in developing countries and geopolitical anxieties push policymakers to favor energy affordability and reliability over aggressive decarbonization.