Yielding to Shortage: Gulf Crisis Prompts Fertilizer and Food Shocks

When transportation insurance withdrew from Gulf waters, it triggered an agricultural supply chain shock whose effects will reach crop yields in South Asia, sub-Saharan Africa, and Latin America within a single growing season.

A container ship is seen in the Strait of Hormuz off the coast of Qeshm Island, Iran, April 18. (AP Photo/Asghar Besharati)

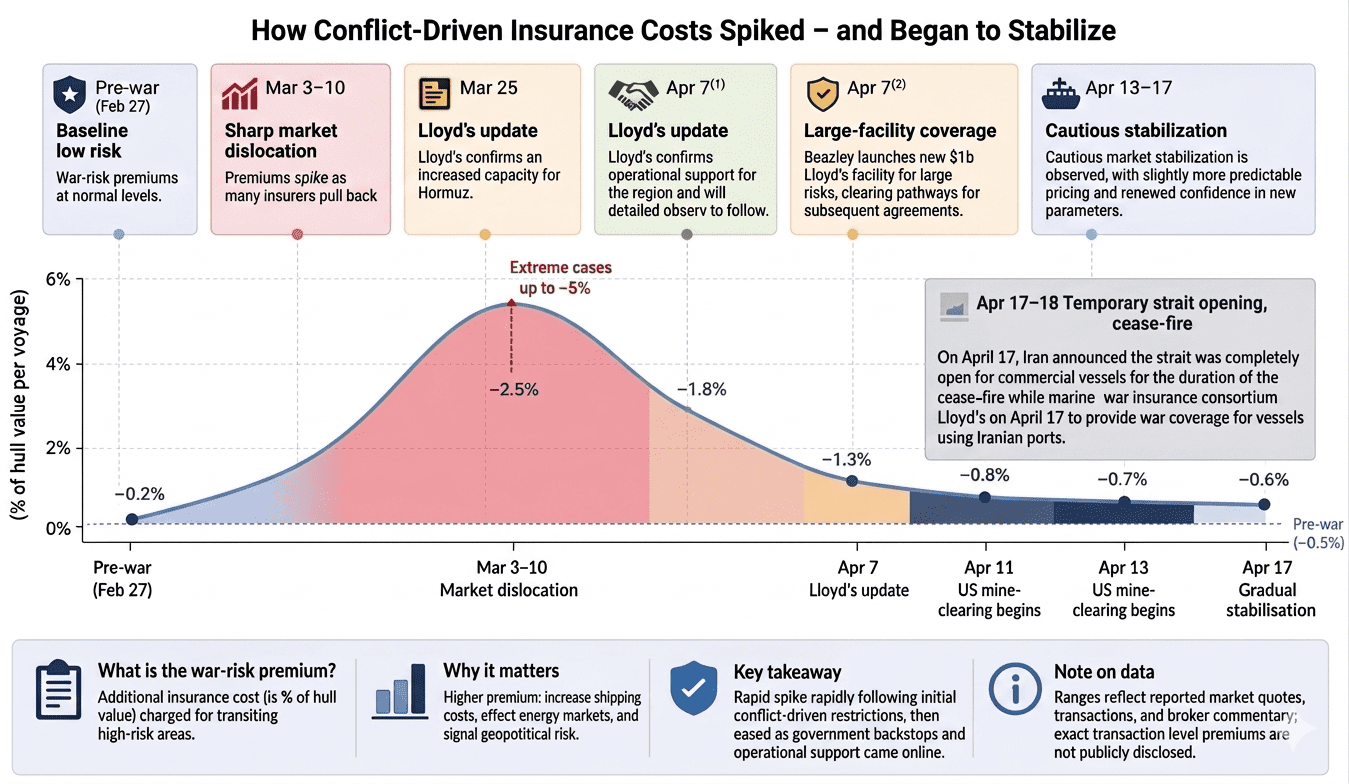

The Strait of Hormuz was effectively closed by an actuary before it was threatened by missiles. The conflict that began February 28 has demonstrated that maritime insurance markets, not kinetic disruption, can be the first mechanism to halt trade, triggering immediate consequences for agricultural supply chains in the Gulf Cooperation Council states and amplifying global food insecurity.

The two-week cease-fire announced April 7, conditioned on Iran’s reopening of the strait, did not normalize insurance conditions, showing how the insurance mechanism operates with a logic and timeline independent of battlefield developments. Subsequent U.S. diplomatic engagement and preliminary discussions involving the U.S. International Development Finance Corporation and insurers have not yet translated into normalized insurance pricing or restored commercial shipping volumes to preconflict levels. The developments of April 17-18 illustrated this gap. On April 17, Iran announced the strait was completely open for commercial vessels for the duration of the cease-fire, triggering a drop of more than 10% in oil prices and a rally in global equity markets. However, shipping companies declined to move: The route declared open covered only about one-third of the full strait due to mines and military blockades still in place, mandatory coordination with Islamic Revolutionary Guard Corps forces was required, and insurance rates remained approximately 300% above preconflict levels, with insurers explicitly not ready to sound the all clear. The opening lasted less than 24 hours: On April 18, Iran reinstated control of the strait in response to the U.S. refusal to lift its naval blockade of Iranian ports. IRGC gunboats fired on at least one tanker near the strait hours after the reclosure announcement. The cease-fire itself expires in just days, and President Donald J. Trump has indicated it may not be extended. Insurance market conditions as of April 18 reflected this volatility: War-risk premiums remained sharply above peacetime baselines, and while Beazley announced a new $1 billion Lloyd’s marine war consortium on April 17 to provide additional hull and cargo war coverage capacity for Strait of Hormuz transits, the April 17-18 cycle of opening and immediate reclosing has not restored market confidence. Insurance constraints will therefore persist until a final and verifiable peace agreement is in place.

Two Crises and One Mechanism

Much of this complexity was already evident in the first days after the outbreak of conflict. Within 48 hours of the initial U.S.-Israeli strikes on Iran on February 28, war-risk premiums for Gulf transit surged fivefold. By March 2, when Iran reiterated in more formal terms its intent to close the strait, marine insurers had issued war-risk cancellation notices and expanded high-risk designations across the Strait of Hormuz and adjacent waters, withdrawing or radically repricing coverage before most missiles had found their targets. Commercial shipping halted not because the waterway was physically blocked but because the financial infrastructure that makes maritime trade legally and operationally possible had been removed. Access to the strait was first constrained by insurance market withdrawal rather than Iranian missiles or a physical blockade. Iranian threats, of course, prompted the removal of that financial infrastructure.

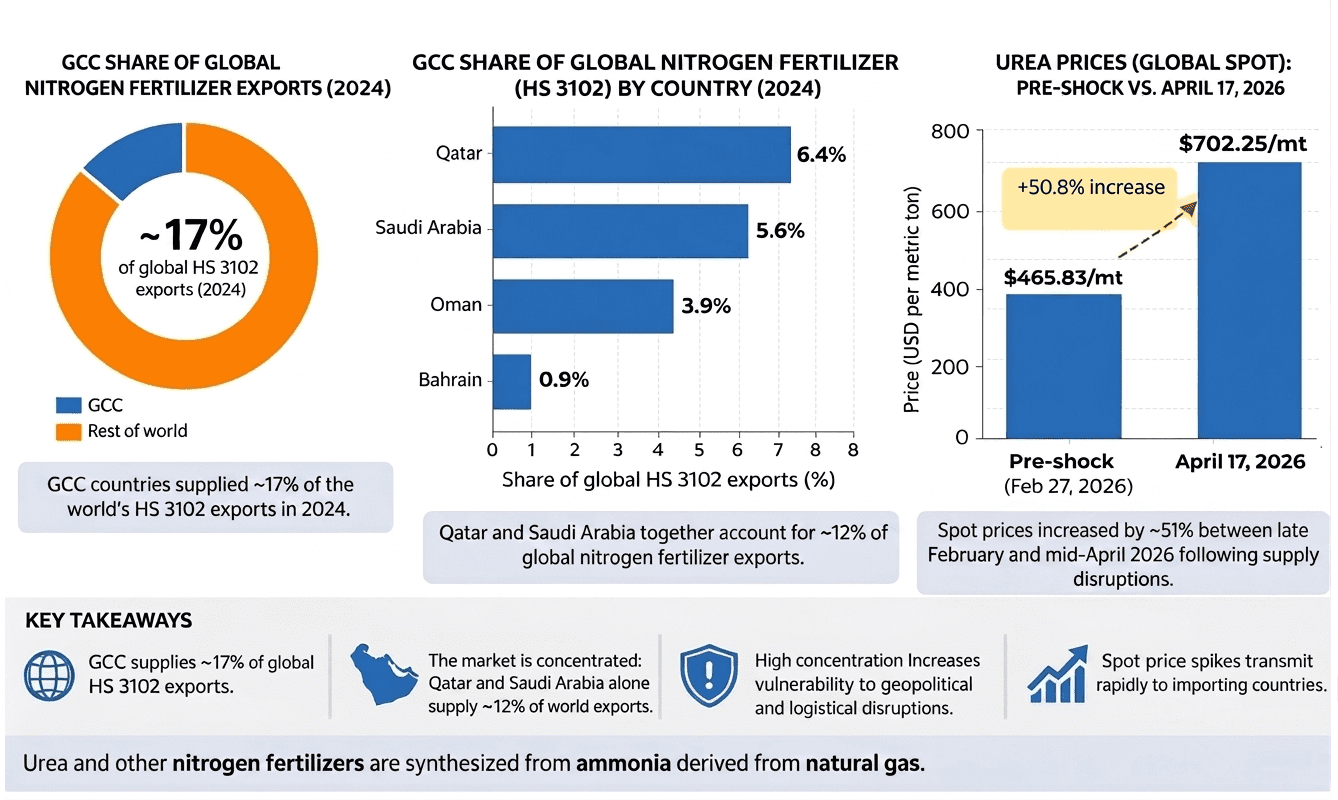

What that closure exposed is a structural vulnerability that current food security policy has systematically underpriced. The Gulf is not merely an oil chokepoint, it is also a major nitrogen fertilizer corridor, as approximately 17% of global nitrogen fertilizer exports, including 46% of global urea flow, originate from the region. This concentration is not incidental: GCC states benefit from abundant, low-cost natural gas, which is the main feedstock for producing ammonia and urea, key nitrogen fertilizers. They also have decades of state-directed investment in fertilizer production capacity. These advantages cannot be quickly replicated elsewhere, which is why a supply shock here cannot simply be offset by other producing regions.

When transportation insurance withdrew from Gulf waters, it did not merely disrupt fuel shipments, it removed a substantial share of the world’s seaborne nitrogen fertilizer supply, including nearly half of global urea from global markets within days, triggering an agricultural supply chain shock whose effects will reach crop yields in South Asia, sub-Saharan Africa, and Latin America within a single growing season.

GCC Fertilizer: Global Concentration and the Price Shock

Sources: United Nations Comtrade; Trading Economics; GPCA (2025) Annual Report

Two distinct crises converged through a single mechanism. The first was an insurance market shock: War-risk cancellations and prohibitive repricing withdrew the financial infrastructure required for commercial shipping, effectively closing the Gulf corridor. The second was a food security crisis of acute and structural dimensions: GCC economies, which import 80% to 90% of their food requirements through the same corridor, faced immediate supply disruption, while the simultaneous collapse of fertilizer exports from the world’s largest urea-producing region set in motion yield consequences that will register across global agriculture. What made this event distinctive was not that these two crises occurred simultaneously but that they operated through precisely the same mechanism, the price-based rationing of maritime access, making them tied in both cause and remedy.

How Insurance Withdrawal Froze the Fertilizer Supply Chain

Commercial shipping requires three insurance layers: hull and machinery coverage for the vessel, protection and indemnity coverage for third-party liabilities, and war-risk coverage for conflict-zone exposure. On March 2, the day Iran declared the Strait of Hormuz effectively closed, the West of England P&I Club announced that its reinsurers had canceled war-risk liabilities for the Gulf and Iranian waters. This reinsurance withdrawal was the first transmission of geopolitical risk into the agricultural supply chain, preceding most missile strikes on production facilities. Reinsurance is the critical backstop for Gulf-focused insurers providing the actual coverage; without reinsurance to protect these insurers against the prospect of catastrophic losses, primary insurers lose the capacity to accept new risks, and insurance underwriting dries up. Without protection and indemnity coverage, vessels could not enter ports; and without war-risk coverage, they could not be chartered. Without cargo insurance, fertilizer shippers could not finance their consignments.

The result was a near-total commercial standstill with Gulf shipping traffic collapsing by around 90% in the first week of the conflict, as ships halted operations, diverted routes, or remained idle, effectively shutting down one of the world’s most critical trade corridors. War-risk premiums for Gulf transit rose from a peacetime baseline of approximately 0.25% of hull value per voyage to a peak midpoint of around 2.5% in the acute phase (March 3-10), stabilizing toward 1.3% to 1.8% after backstop measures were announced, in typical cases and up to 5% to 10% for high-exposure vessels, implying multimillion-dollar costs per voyage for very large crude and bulk fertilizer carriers.

On March 23, the Lloyd’s Market Association indicated that war-risk insurance remained technically available for Strait of Hormuz transit, but operational risks, particularly crew safety, and sharply rising premiums became the binding constraints on shipping activity.

Both prohibitive pricing and nominal availability produce the same result for fertilizer supply chains, as shipments do not move. The crisis has triggered a “permanent repricing event” for marine war risk, with tighter contract conditions expected to persist beyond the immediate conflict. The war-risk repricing mechanism did not only freeze shipping but also translated directly into food system consequences that registered across global food systems within weeks.

Strait of Hormuz War-Risk Premium Escalation Timeline

Sources: Lloyd’s Market Association; Howden Re; Reuters; West of England P&I Club; The Wall Street Journal; U.S. International Development Finance Corporation

From Insurance Freeze to Global Food Insecurity

The disruption triggered by the insurance market shock has had immediate and far-reaching implications for global food systems. At current levels, the sustained interruption of Gulf exports could remove up to 4 million metric tons of fertilizer per month from global supply.

The impact is highly asymmetric. India and China, which account for approximately 28% and 23% of GCC petrochemical exports respectively, are among the world’s largest producers of nitrogen-intensive crops. A sustained supply shortfall to either market would translate, within a single growing season, into reduced yields of corn, wheat, and rice, the staple crops underpinning global food security.

The disruption also feeds back to the Gulf itself, highlighting the structural paradox at the heart of GCC food security. The GCC states simultaneously dominate global fertilizer exports and depend on the same maritime corridor for 80% to 90% of their own food imports. The collapse of shipping flows therefore threatens both the region’s economic role as the world’s nitrogen corridor and its nutritional security as a food-importing region. The resilience of the Strait of Hormuz is not merely a trade concern; it is a precondition for the region’s continued ability to feed itself.

Farmers facing nitrogen shortfalls have few options for dealing with limited nitrogen supplies. They can reduce application rates, switch to less nitrogen-intensive crops, such as legumes, or abandon marginal land. Each entails yield losses and aggregate production declines. The most acute impacts are likely to register in South Asia and sub-Saharan Africa, where smallholder farmers have limited access to alternative inputs and where wheat and rice yields are already under stress. A sustained disruption lasting one planting cycle – roughly three to four months for winter wheat in northern India and Pakistan – is sufficient to produce measurable harvest shortfalls. The downstream effects, including price spikes in staple grain markets and reduced caloric availability in low-income import-dependent countries, would follow within six to 12 months of the initial supply disruption.

Addressing Both Crises at Their Shared Root

GCC policymakers and their partners in the United States and United Kingdom – governments and institutions that possess the sovereign investment capacity, insurance-market relationships, and diplomatic leverage to act quickly – are best positioned to respond to these crises.

Two priorities stand out as both feasible and immediately deployable if the Strait of Hormuz remains closed. First, GCC governments, in coordination with the United States and United Kingdom, can activate targeted war-risk support instruments to restore minimum insurability for food and fertilizer cargoes. This means deploying U.S. International Development Finance Corporation cargo guarantee facilities, which can backstop up to 50% of insured value for qualifying agricultural supply shipments under its existing food security mandate. The International Development Finance Corporation already launched a $40 billion war-risk reinsurance facility with several major U.S. insurers, including Chubb, AIG, and Berkshire Hathaway. However, its current focus is energy shipments, and it will need to explicitly extend coverage to food and fertilizer cargoes. GCC government can also coordinate with UK Export Finance and equivalent GCC export credit agencies to offer sovereign reinsurance capacity for the highest-exposure vessel classes transiting the Strait of Hormuz and convene an ad hoc Lloyd’s-market reinsurance pool, modeled on precedents from the Iran tanker crisis of 2019, to restore baseline war-risk availability at premiums below the 1.5% of hull value threshold above which most commercial operators cease voyaging. The policy objective is not to eliminate war-risk pricing but to keep it below the threshold at which shipping halts. This pathway, however, depends on U.S. political willingness to activate food security mandates in a geopolitical context that may complicate such coordination. If U.S. participation isn’t possible, GCC sovereign wealth funds and the Islamic Development Bank are alternative capitalization vehicles for equivalent backstop instruments. Recent International Development Finance Corporation negotiations with major U.S. insurers did not produce binding backstop commitments, underscoring the urgency of activating these instruments while the strait remains closed.

Second, GCC states should build strategic food reserves in accessible partner countries, backed by prearranged priority logistics contracts. The target should be a minimum 90-day buffer for staple commodities, wheat, rice, and edible oils, held in bonded storage facilities in diversified locations, including Turkey, India, and East African port hubs, all accessible via routes that don’t pass through the Strait of Hormuz. The 90-day period is estimated to cover the duration of acute disruptions – the 2019 Gulf tanker crisis and 2022 Black Sea disruptions both resolved within roughly that window – and aligns with the World Food Program’s standard minimum buffer for food-insecure populations. These reserves should be funded through existing sovereign wealth and investment platforms and paired with prenegotiated charters with major bulk shipping operators to guarantee delivery priority in the event of the Strait of Hormuz’s closure. This approach avoids the long lead times of infrastructure investment, builds on established sovereign platforms, and can be operationalized within 12-18 months. Some GCC states, notably the UAE, have already established domestic strategic reserves, including grain storage at Fujairah port, as well as food security arrangements with partner countries, including agricultural investments in Romania, Serbia, and Ukraine and a $7 billion food corridor with India. Saudi Arabia, through its sovereign agribusiness SALIC, holds overseas agricultural investments in Ukraine, Canada, Brazil, and Australia and benefits from Red Sea port access at Jeddah and Yanbu that fully bypasses the Strait of Hormuz, and the kingdom holds the deepest reserves in the Gulf. Oman’s ports at Duqm, Salalah, and Sohar also sit outside the strait and could serve as regional redistribution hubs, though several were struck by drones during the current crisis, limiting their near-term utility. Qatar, through its sovereign investment arm Hassad Food, has agricultural assets in Australia, Sudan, and Argentina and has achieved near self-sufficiency in dairy and vegetables since the 2017 boycott, though it remains heavily dependent on the Strait of Hormuz for grain imports. Kuwait and Bahrain have the most limited arrangements and remain the most exposed, with few alternative resupply routes; and even the Emirati, Saudi, and Omani arrangements ultimately rely on global maritime supply chains that have been subject to war-risk repricing.

In crisis conditions, restoring continuity of access is more achievable than redesigning the system itself. The priority is therefore to keep trade flows moving at reduced but viable levels while it may not be possible to eliminate underlying vulnerabilities.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

One silver lining of the Iran conflict may be the emergence of new, more durable foundations for regional economic integration via more agile trade corridors in the Gulf and beyond.

The longer the conflict lasts, and the more damage to energy facilities, the greater the risk of oil market tightness, rising prices, and stranded commodities.

As the Gulf countries transition to a new energy order, creating “good jobs” in high-value export-oriented services that provide citizens with adequate benefits, economic security, and career ladders will help these economies diversify and achieve increased growth.

Regional sovereign wealth funds are increasingly focusing on sustainability, mobilizing resources for investments in alternative energy projects and demonstrating an alignment with their respective government’s strategy for the energy transition.