The King Abdullah Financial District during late noon hours in Riyadh, Saudi Arabia, August 29. (REUTERS/Hamad I Mohammed)

Saudi Arabia’s ambitious economic and social reforms under Vision 2030 have now entered their 10th year. Reform implementation has been impressive. The “Vision 2030 2024 Annual Report” found that 80% of the key performance indicators established under the Vision Realization Programs have been achieved and a further 13% are on track to be met.

Despite the high reported success rate in meeting the key performance indicators, it is not easy to get a clear picture of how the reforms are affecting the day-to-day workings of the Saudi economy and whether they are translating into improved economic performance. The annual average growth rate of real non-oil gross domestic product has actually been weaker post-Vision 2030 (2017-24) than pre-Vision 2030 (2007-15) and oil revenue remains the key driver of the Saudi economic cycle. Further, the fiscal and current account balances were in large surplus during 2007-15 but have been in deficit (fiscal) and smaller surplus (current account) on average during 2017-24.

Macroeconomic variables, such as growth, fiscal and external balances, and inflation, however, are influenced by many things in addition to the reforms, including factors that are beyond the control of Saudi policymakers, such as oil prices and U.S. monetary policy. The Brent oil price averaged $88 per barrel during 2007-15 compared to $71/bbl during 2017-24, and the U.S. federal funds rate averaged less than 1% during 2007-15 compared to 2.2% during 2017-24. Underlying economic conditions were more favorable for Saudi Arabia in the period before Vision 2030 than they have been since.

Given the many factors that affect macroeconomic performance, it is difficult to infer too much about the success or otherwise of the reforms from broad aggregates, such as growth, unless a very careful statistical analysis is conducted that adequately controls for the many different factors that influence the growth outcome. Therefore, monitoring indicators that capture narrower aspects of the economy that are more directly influenced by the Vision 2030 reforms is useful. In past analysis, four indicators were highlighted: the female participation rate and employment; the number of foreign visitors and their spending; foreign direct investment inflows; and educational outcomes of Saudi students. A fifth indicator is added here – the growth of reexports to measure progress in developing the logistics sector. Each of these indicators speaks directly to a key area of the Vision 2030 reforms.

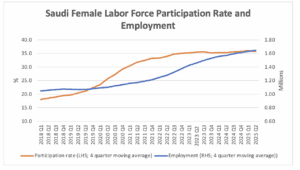

Higher Female Employment, But Gains in the Participation Rate Have Stalled

The Saudi female labor force participation rate – the share of Saudi women of working age who are employed or seeking employment – doubled to nearly 35% between 2017 and 2021, but it has been stuck in the 35%-36% range since. Saudi female employment has continued to grow, rising by 160,000 or close to 11% over the past two years, more than twice the gain in Saudi male employment. This employment growth has resulted in a sharp drop in the Saudi female unemployment rate from 15.9% in the second quarter of 2023 to 11.3% in the second quarter of 2025 (equivalent male rates: 4.6% to 4.3%). At the same time, the average wage paid to Saudi women rose by 17%, nearly twice the rate of increase for Saudi men (although Saudi women, on average, get paid only two-thirds of the male wage).

Source: General Authority for Statistics

The increase in the female participation rate and employment is due to the reforms that have been undertaken to encourage women to join the labor force. These include changes to the guardianship system, legal reforms that have reduced segregation in the workplace and banned discrimination, the introduction of government programs to defray travel and child care costs, and permitting women to drive. The increase in the participation rate may also be partly due to changes in the way the labor force survey is conducted. During the coronavirus pandemic, the survey switched from in-person to over-the-phone interviews and the female participation rate jumped by 7 percentage points during 2020 (from 25.7% to 32.8%). The change to phone interviews may have resulted in a higher proportion of women responding to the survey and potentially a more accurate recording of their participation in the labor market (in other words, participation rates may previously have been underreported because men usually responded to the in-person interviews).

While the continued growth in female employment is good news, the question is why the female participation rate has stayed in the 35%-36% range. This is still well short of the G20 average of 51% – only India has a lower female participation rate than Saudi Arabia among G20 countries. It may be that the easing of the legal, social, and cultural constraints that women faced in the past has an impact on the participation rate in waves. There may have been a group of women who were ready to enter the labor market as soon as the restrictions were eased, but others may be waiting to see how the changes translate to employment conditions on the ground before deciding what to do. If the unemployment rate continues to decline and wages to rise, this may provide more incentive to these women to enter the labor market.

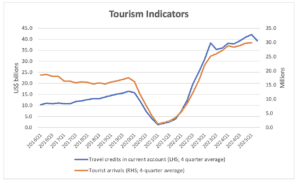

More Foreign Tourists Are Visiting Saudi Arabia

The tourism sector continues to grow, albeit at a slower pace than in 2022-23. The number of foreign visitors to the kingdom averaged close to 30 million on an annual basis in the first quarter of 2025, representing growth of 3.8% compared to the first quarter of 2024. Spending by foreign tourists totaled just under $40 billion in the year to the second quarter of 2025, some 4% higher than in the corresponding quarter of 2024. The slowdown in growth is not surprising given that the rapid increase during 2022-23 was driven by the reopening of the country after the coronavirus pandemic and the surge in entertainment events hosted in the kingdom.

Sources: Saudi Central Bank; Ministry of Tourism

Foreign visitors to Saudi Arabia are predominately from Muslim countries. Bahrain, Egypt, Kuwait, and Pakistan together accounted for around 11 million of the 29 million tourists in 2024. Many of these people are visiting for religious purposes, although an increasing number are coming to visit family or for tourism. Visitors from Western Europe and the Americas doubled between 2022 and 2024 to 3 million and accounted for 10% of arrivals.

Growth in tourism is settling to a more sustainable pace, and continued impetus to the sector’s development will come from several sources. These include the opening of newly developed resorts and hotels, particularly on the Red Sea coast, the upcoming operational debut of the new airline, Riyadh Air, which will improve flight connections to the kingdom, and the hosting of global and regional events, such as the Asian Winter Games, Expo 2030, and the 2034 World Cup.

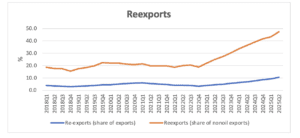

The Logistics Sector Is Growing

Saudi Arabia is well positioned geographically to fulfill its goal of becoming a regional and global logistics hub, but it faces stiff competition from the United Arab Emirates and Qatar. Official data suggests that considerable progress is being made in developing the logistics sector. Reexports – goods that are imported and then “reexported” without alteration – is one indicator of the size of the logistics sector. Reexports have tripled since the beginning of 2022 with most (over 60%) heading to the UAE and appearing to mainly comprise mechanical and electrical equipment.

Source: General Authority for Statistics; author calculations

Policies to develop the logistics sector have focused on improving the port, airport, and general transport infrastructure and increasing the efficiency of custom clearance procedures to enable the rapid processing of goods and people entering the kingdom. The value of imports and non-oil exports moving through the kingdom’s airports has increased noticeably over the past two years. Nevertheless, it is hard to pin down a precise reason for the surge in reexports to the UAE.

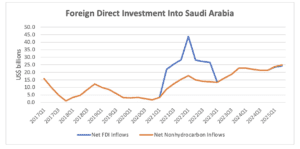

Foreign Direct Investment Is Increasing

Foreign direct investment inflows into the nonhydrocarbon sector in Saudi Arabia are on an upward trend, though this is not immediately apparent in the official data for two reasons. First, sales by Saudi Aramco of stakes in an oil and a gas pipeline to consortiums of international investors in 2021 and 2022 boosted aggregate FDI inflows in these years. While these investments are important because they free capital on Aramco’s balance sheet for other uses, they do not directly help meet a key goal of Vision 2030, namely a more diversified economy. Second, the preliminary quarterly data published by the statistical authority tends to underestimate FDI inflows relative to the final data, which is based on more comprehensive information. Therefore, data published for the first two quarters of 2025 will likely be revised higher when fuller information becomes available. Adjusting for these factors and using a four-quarter moving average to reduce quarter-to-quarter volatility in the data suggests that nonhydrocarbon FDI has been on a trend increase since late 2021, reaching $25 billion in the year to the second quarter of 2025.

Source: General Authority for Statistics; author calculations. Note: For nonhydrocarbon inflows, sales of oil and gas pipelines by Aramco to international investors in 2021Q2 and 2022Q1 are excluded and data for 2025Q1 and 2025Q2 are adjusted upward by the average revision to the preliminary data in 2024. All data shown is the sum of the previous four quarters.

Given several recently announced investment deals in artificial intelligence, technology, and finance, the announcement of a new property ownership system that should broaden permissions and clarify regulations for non-Saudis who want to own real estate in the kingdom (expected to come into effect in early 2026), and ongoing reforms to improve the investment environment, FDI inflows into the nonhydrocarbon sector should continue to increase. The $11 billion deal involving the lease and leaseback of Aramco’s Jafurah gas processing facilities with a consortium of international investors will boost aggregate FDI inflows when it is completed but will not directly affect the nonhydrocarbon sector.

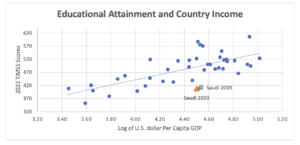

Educational Outcomes Are a Cause for Concern

The results from the 2023 “Trends in International Mathematics and Science Study” were not encouraging for Saudi Arabia. The study is conducted every four years and presents standardized questions on mathematics and science to 4th- and 8th-grade students in participating countries. It is a useful barometer of relative educational achievement. Saudi students ranked near the bottom of the 41 countries covered in the 2023 study and showed little improvement from the 2019 study despite efforts to upgrade and modernize the educational system in the kingdom. Girls continued to score significantly better than boys in the science tests, but there was little gender difference in the mathematics scores.

Sources: Trends in International Mathematics and Science Study, 2019 and 2023; International Monetary Fund; author calculations. Notes: The TIMSS scores is the average of the 8th-grade science and mathematics score for each country. Saudi Arabia is represented by the orange triangle (2023) and green square (2019).

Given the long lags that are involved in improving educational outcomes, it is perhaps not surprising that progress has so far been limited. While other ways are being pursued to provide high quality education to Saudi students, including through the international scholarship program, this is only available to a subset of higher performing students. Ultimately, outcomes in the domestic school system will need to improve if the goals of Vision 2030 are to be met. This will require continued focus on strengthening teacher quality and ensuring that a robust curriculum is taught in schools to provide students with the skills needed to thrive in the economy that Saudi Arabia is trying to build. Better quality education is also essential to attract high quality talent and companies to the kingdom. Without good schooling for their children, workers will be reluctant to relocate to the country.

Structural Reforms, Not High Government Spending, Key to Progress

The Vision 2030 reforms are continuing to drive improved outcomes in many areas of the Saudi economy. Substantial progress has been made in engaging Saudi women in the labor market and developing the tourism sector, although gains in these areas have slowed. Efforts to boost FDI inflows and develop the logistics sector are making headway, but reforms to improve educational attainment are yet to bear fruit.

Regulatory and legal changes and the greater use of technology have played a significant role in the four areas where progress is evident. For example, the decision to start issuing tourist visas in 2019 is the single biggest driver of the growth in tourism; giving women the ability to work and own a business without the consent of a male guardian has been very important in boosting female employment; and the application of technology has enabled faster customs clearance and business license issuance. The lesson is that, while large-scale government investment is needed in some areas (infrastructure, for example), there is much that can be achieved through the consistent and transparent implementation of traditional “structural” reforms that focus on getting the legal, regulatory, and government incentive structure right in the economy. This is good news as a period of low oil prices that necessitates lower government spending need not derail economic momentum.

In the long run, the Vision 2030 reforms will not be fully effective unless productivity is increased. Higher productivity is critical if the new industries that are being developed in the kingdom are to compete successfully in global markets. Better educational outcomes are critical for higher productivity. Again, improving educational outcomes should not involve significant new outlays as the government budget already spends heavily in this area. Improved quality, not quantity, of spending is needed.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

Payments by Aramco are still the key driver of government revenue in Saudi Arabia despite the notable increase in non-oil revenue, particularly from the value-added tax, in recent years.

As the Gulf countries transition to a new energy order, creating “good jobs” in high-value export-oriented services that provide citizens with adequate benefits, economic security, and career ladders will help these economies diversify and achieve increased growth.

Positive developments in four indicators during 2024 – the female labor force participation rate, tourist arrivals, foreign direct investment inflows, and student educational attainment – will give confidence that the bold diversification plans underway in Saudi Arabia are on track.

If the memorandum of understanding between the United States and Iran holds, the Saudi economy will grow strongly in the second half of 2026 and into 2027.

The Saudi budget recorded a large deficit in the first quarter of 2026 as spending surged, but higher oil revenue during the rest of the year should limit the size of the annual fiscal deficit.

Business conditions in the Gulf generally improved in April, but they remained weaker than before the Iran war. There are signs that price pressures are increasing as the conflict impedes trade.

On January 8, AGSI hosted a virtual roundtable with its leadership and scholars as they look ahead and assess trends likely to shape the Gulf region and U.S. foreign policy during the coming year.