Will the U.S.-Iran Conflict Reshape Global Energy Flows and Shipping?

The longer the conflict lasts, and the more damage to energy facilities, the greater the risk of oil market tightness, rising prices, and stranded commodities.

Fire and smoke rise in the Fujairah oil industry zone, caused by debris after interception of a drone by air defenses, according to the Fujairah media office, amid the U.S.-Israel conflict with Iran, in Fujairah, United Arab Emirates, March 4. (REUTERS/Amr Alfiky)

In response to the coordinated U.S. and Israeli airstrikes that began February 28, Iran has sought to shift the cost of the conflict by targeting Gulf Arab states, likely to induce its neighbors to press the United States to de-escalate. The strategy may backfire should the Gulf Arab states decide it is more cost effective to more actively support the campaign than endure the risk and cost of sustained missile and drone barrages.

Iran sought to signal potential costs of a regional conflict on the energy-exporting Gulf states by threatening to close the Strait of Hormuz. Before the start of the conflict, the Islamic Revolutionary Guard Corps announced a temporary closure of the Strait of Hormuz for a naval exercise. On February 28, the IRGC began using radio broadcasts to inform tankers that they could not pass through the strait. Though Iran did not conduct direct naval actions to fully close the Strait of Hormuz, traffic through the 21-mile-wide waterway (at its narrowest point) reduced to a trickle within days.

Even before the launch of military operations February 28, the markets began pricing in the risk of conflict in the Gulf – seen in the steady increase in the price of crude oil and shipping rates. Since shipping is the most efficient way to move large amounts of crude oil, liquefied natural gas, and other hydrocarbons, any discussion of the effects of this conflict on energy markets must include commercial shipping: The movement of billions of barrels of oil and metric tons of LNG from production facilities to markets requires open and safe waterways. The Strait of Hormuz and Suez Canal are the world’s most important arteries for moving oil and gas. The hostilities have already reduced traffic through both waterways, increased shipping and insurance rates, and raised the price of oil. The longer the conflict lasts, and the more damage to energy facilities, the greater the risk of oil market tightness, rising prices, and stranded commodities. Over time, sustained crude oil price increases will also result in higher prices on gasoline and many other consumer products.

Iranian Production

Iran only produces 3.3 million barrels per day of oil, around 3% of the world’s supply. Saudi Arabia leads OPEC+ oil producers at 34%, followed by Iraq at 15%, the United Arab Emirates at 12%, and Kuwait at 9%. Since Iran is subject to multiple sanction regimes, around 90% of its crude oil goes to China at significant discounts, sold illicitly in violation of sanctions. Decades of these sanctions degrading Iran’s oil sector combined with aging fields that produce less oil over time have nearly halved Iran’s ability to extract oil at the 6 mb/d level it maintained in the 1970s. Given that limited Iranian production, the impact to global markets of taking Iran’s crude production offline would be limited.

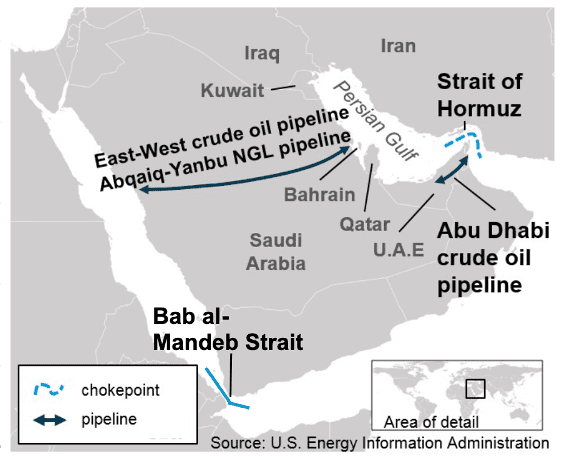

Trade Routes

Source: U.S. Energy Information Administration

While a reduction in Iranian exports is unlikely to roil international markets, Iran holds greater potential to disrupt international energy markets by threatening exports from its neighbors. Iran’s location on the Strait of Hormuz and its influence over the Houthis near the Red Sea grant it an outsized role in global energy markets. Saudi Arabia, Iraq, Kuwait, Iran, and the UAE ship about 25% of the world’s crude through the Strait of Hormuz. In 2025, tankers moved about 16.7 mb/d of oil and condensate, with most of the shipments heading to Asia. Furthermore, around 20% of the world’s LNG, led by Qatari exports, also passes through this waterway. By March 1, oil tanker traffic through the strait declined 98% from an average 14 mb/d to 250,000 b/d.

Saudi Arabia can bypass the Strait of Hormuz via the Abqaiq-Yanbu pipeline system (East-West Crude Pipeline or Petroline), and the UAE can turn to the Abu Dhabi Crude Oil Pipeline, albeit at reduced volumes. The Abqaiq-Yanbu pipeline can only move around 5 mb/d, below the 7.3 mb/d Saudi Arabia is exporting. The Abu Dhabi Crude Oil Pipeline can move up to 1.8 mb/d, below the 2.85 mb/d it exported in 2025. No alternative routes exist for oil exports from Bahrain, Kuwait, and Qatar. There are no alternatives for moving LNG out of the region, a problem for Qatar, as LNG makes up 45% of its petroleum product exports.

In January, Saudi Arabia, Kuwait, the UAE, and Iraq began increasing their combined oil exports by nearly 600,000 b/d to hedge against supply disruptions in the Gulf. Saudi Arabia increased oil exports by 13% year-on-year to 7.3 mb/d, with the UAE, Iraq, and Kuwait making up another 1.52 mb/d for the first 24 days of February. Saudi Arabia also increased oil exports before the June 2025 U.S.-Israeli strikes on Iran and then reduced supply as the risk of a wider conflict declined. During the March 1 OPEC+ meeting, members agreed to a 206,000 b/d increase in monthly production beginning in April, a higher volume than the incremental 137,000 b/d monthly increase in the fourth quarter of 2025.

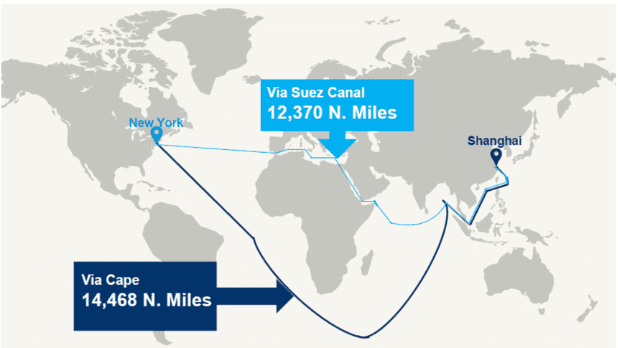

The Suez Canal also plays an important role in energy security and global trade, with around 30% of global container traffic passing through the waterway as well as approximately 8% of LNG and 9% of seaborne oil. The Suez Canal serves as a key artery delivering Middle Eastern oil and LNG to Europe. The October 2023 attacks on commercial shipping by Iran-allied Houthis prompted a 50% decline in oil tanker traffic, dropping from 7.9 mb/d to 3.9 mb/d. As attacks continued from 2023-24, companies diverted ships through the longer Cape of Good Hope – Egypt suffered economic losses, global shipping capacity shrank by around 20%, and shipping rates surged. While the Houthis have indicated an intention to resume attacking Red Sea shipping in response to the U.S.-Israeli strikes on Iran, they have not yet launched attacks. Nonetheless, Maersk halted its Trans-Suez routes as of March 1.

Source: Lloyd’s List, Kuehne+Nagel, sea explorer, Reuters, CNBC, US Department of Defense

Damage to Shipping and Energy Infrastructure

The February 28 U.S.-Israeli attack on Iran has sparked a conflict far more severe than the 12-day war in June 2025. Iran has struck targets in Israel, the UAE, Qatar, Bahrain, Oman, Saudi Arabia, Jordan, and Kuwait, expanding the scope of hostilities. Since February 28, shipping traffic through the Strait of Hormuz has declined by 70%, with Maersk, Hapag-Lloyd, CMA CGM SA, and MSC all suspending vessel traffic through the waterway. On March 1, projectiles damaged three oil tankers near the Strait of Hormuz, while President Donald J. Trump announced the U.S. Navy sank nine Iranian ships. He also announced, without providing significant detail, the possibility the United States would escort foreign-flagged ships through the strait. This announcement is unlikely to ease shipping companies’ concerns and will instead incur additional U.S. government expense while drawing pushback from U.S. Navy leadership.

Strikes have also targeted energy facilities. Iran’s Mehr News Agency reported explosions on Kharg Island, the country’s main oil export terminal on February 28. On March 2, Iranian drones attacked Qatar’s natural gas hub at Ras Laffan, Saudi Arabia’s biggest oil refinery at Ras Tanura, and a power station south of Doha. Qatar Energy temporarily halted LNG production and Aramco paused crude processing.

Global Markets Rattled

Financial markets have reacted to the conflict. The price of oil rose 9% to $79 per barrel March 2, a six-month high. Natural gas futures surged by 50%, as Qatar halted LNG production. Abu Dhabi closed its stock exchange for two days, likely to limit panic selling. The yield on U.S. Treasuries grew, which means higher borrowing costs for consumers on mortgages as well as auto and business loans. Shares of oil majors, such as Exxon, Chevron, BP, and Shell, all rose.

Reshaping Global Energy and Trade Flows

The length and scale of destruction of this latest conflict will determine how it reshapes global energy and trade flows. The first few days of the conflict led to increases in the price of oil as well as the cost of shipping and insurance. A protracted conflict will likely result in inflation in advanced economies, an increase in the cost of gasoline, and escalating expenses for airline, trucking, and shipping operations. The Qatari economy will likely suffer due to the inability to bring LNG to the market, and Egypt will feel the revenue loss from ships avoiding the Suez Canal. Furthermore, prolonged security risks to shipping through the Strait of Hormuz and Suez Canal will cut off spare crude oil production capacity to meet global energy demand, around 60% of which exists in Saudi Arabia.

The intensity and scope of Iran’s response seem to be focused on enlisting worried Arab neighbors to pressure the United States to de-escalate. There is the possibility these Iranian actions may backfire if Iran’s Gulf neighbors become so outraged by the attacks that their strategic calculus turns against support for diplomatic pressure on the United States and Israel and instead gives them time to finish the war on their terms. It would be ironic if the tactics Iran settled on to enlist their reluctant but vital support for ending the war persuaded Gulf states that continued U.S.-Israeli military action would end the conflict more quickly and be more cost effective than repelling Iranian missiles and drones. For now, Gulf states continue to mull over the costs and benefits of moving from defense to retaliation.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

There was a growing war risk premium in the oil markets tied to escalating regional tensions; the shift from shadow confrontation to direct military action changes the calculus.

Gulf Arab countries urged the United States not to strike Iran, but now that is happening, they are in danger of being sucked into a conflict they cannot control but that will likely reshape their present and future realities.

From the Gulf to the eastern Mediterranean and North Africa, governments are recalibrating fiscal terms, monetization strategies, and partnership models to attract international players.