OPEC Extends Cuts but Market Uncertainties Remain for 2018

OPEC and its non-OPEC allies reached an agreement at their November 30 meeting in Vienna to formally extend production cuts to the end of 2018 with the deal subject to review at a biannual meeting in June. The parameters of the agreement remain the same, with the coalition of 24 OPEC and non-OPEC participating countries...

Russian Energy Minister Alexander Novak and Saudi Minister of Energy, Industry, and Mineral Resources Khalid al-Falih attend a news conference after OPEC's meeting in Vienna, Austria, Nov. 30. (AP Photo/Ronald Zak)

OPEC and its non-OPEC allies reached an agreement at their November 30 meeting in Vienna to formally extend production cuts to the end of 2018 with the deal subject to review at a biannual meeting in June. The parameters of the agreement remain the same, with the coalition of 24 OPEC and non-OPEC participating countries maintaining production cuts of 1.8 million barrels a day (mb/d) in an effort to reduce global inventories to the targeted five-year average level. This is the second extension from the original June 2017 expiration given the much slower than anticipated rebalancing of oversupplied markets. The post-meeting communique noted that “the market rebalancing has gathered pace since May, with the OECD stock overhang falling to around 140 million barrels (mb) above the five-year average for October, a drop of almost 140mb since May,” but a further drawdown of 150 million barrels was needed to bring inventories to within the five-year average range.

With the outcome in Vienna in line with market expectations, benchmark oil prices have come off the more than two and a half-year highs posted in November. The easing of prices in part reflects a lower political risk premium based on the de-escalation of tensions in Iraq and an end to the harsh rhetoric between Saudi Arabia and Iran.

Equally, with the OPEC meeting behind them, analysts have shifted their focus to the wide range of uncertainties underpinning the market outlook in 2018, and especially the upcoming seasonally weaker first quarter demand period. The scale of the U.S. shale supply response to recent higher price levels, the strength of global oil demand, and heightened political risk in major oil producing countries are the main uncertainties influencing oil market sentiment. Saudi Arabia’s Minister of Energy, Industry, and Mineral Resources Khalid al-Falih acknowledged a “number of variables that we cannot fix with certainty going into the new year.”

Uncertain Price Outlook

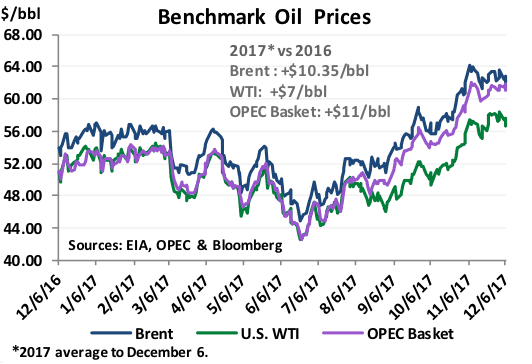

In sharp contrast to the more than $8 per barrel (/bbl) increase in the days following the historic 2016 meeting, oil prices are largely unchanged from pre-meeting levels this time around. International Brent crude was last trading at around $62/bbl, U.S. West Texas Intermediate at $56.70/bbl, and the OPEC Basket at $61/bbl. Going forward, analysts are divided on the outlook for oil price direction. Some industry experts believe the traditionally weaker winter demand period and rising non-OPEC supplies hold the potential to undermine current market strength in the first half of 2018, and fear a repeat of 2016 when prices plummeted by around $12/bbl from January highs to June lows. Other analysts argue the strong resolve to maintain unity and the renewed commitment to supply cuts that emerged from the Vienna meeting will provide a stronger-than-expected foundation for oil prices in 2018. These analysts singled out the group’s pledge to remain “agile and responsive” to uncertain market developments as a key factor supporting a more sanguine market sentiment.

The unexpected inclusion of Nigeria and Libya into the production fold is also seen as removing a potential downside risk to prices next year. Both strife-torn countries were exempted from the original agreement but they have now pledged not to increase production above their peak levels reached in 2017, which effectively caps Libya’s production at 1 mb/d and Nigeria’s at 1.8 mbd.

Potential for Lower Production in 2018

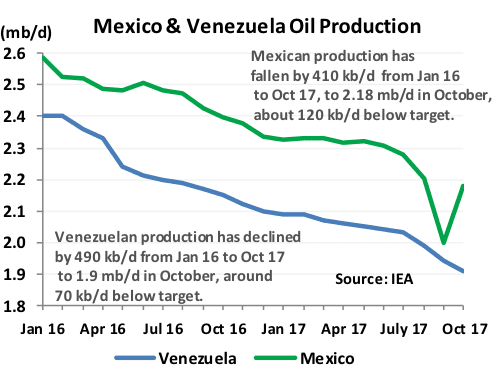

At the same time, the alliance may see supply cuts far exceed the targeted 1.8 mb/d in 2018 due to involuntary production losses, political turmoil, natural field decline, and improved compliance. Production in Venezuela and Mexico has fallen below allocations this year. The latest data for October pegs production in Venezuela 60,000 barrels per day (kb/d) below its target, while Mexico posted a steeper 120 kb/d. Production from the two countries could fall by a combined 300 kb/d in 2018. Mexico has been struggling with declining output for years, with production forecast to fall by a further 110 kb/d next year, to 2.14 mb/d against its official target of 2.3 mb/d.

Venezuelan output in October hit three-decade lows in the wake of the severe financial crisis and U.S. sanctions, with output plummeting by 180 kb/d from January to October. The decline in Venezuelan production has accelerated in recent months following the imposition of new U.S. sanctions, with October output at 1.91 mb/d versus its quota of 1.97 mb/d, according to the International Energy Agency. Analysts expect Venezuelan production to fall by an additional 200 kb/d in 2018.

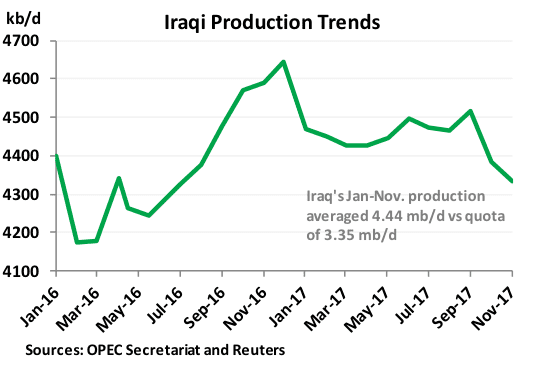

Iraq’s noncompliance has also rankled OPEC officials this year but may now be a nonissue after civil unrest and the capture of the oil-rich Kirkuk region by Iraqi forces led to the shut-in of some 300 kb/d of production. Baghdad has increased southern exports to partially offset the loss from the north, with November output estimated at around 4.33 mb/d. Production is expected to remain at reduced levels close to the country’s target of 4.35 mb/d while Baghdad and Erbil negotiate who controls sales and revenue of northern exports to the Turkish port of Ceyhan on the Mediterranean. Baghdad is demanding that Iraq’s State Organization for Marketing of Oil handle all of the northern sales from the Kurdish region but so far there have been no serious discussions on the issue and the stalemate may continue for another six months, until after Iraq’s parliamentary elections in May. As a result, Iraq may be more compliant with its target in 2018, or at least in the first six months of the year.

OPEC and its partners overall have achieved exceptionally strong adherence to the pledged targets so far in 2017 but several countries, especially Saudi Arabia, have made greater cuts to offset weaker compliance by others, including Iraq and the United Arab Emirates. In a post-meeting briefing Falih said he would be “breathing down the necks” of countries to ensure they meet their commitments. Falih’s term as OPEC president ends this month with the role rotating to UAE Minister of Energy Suhail Mohamed Faraj Al Mazrouei for 2018. Falih is nonetheless expected to continue exerting strong leadership next year with his new appointment as chair of the Joint Ministerial Monitoring Committee, along with Russian Energy Minister Alexander Novak as vice chair. The UAE has been a weak link in the agreement, curtailing production by only about two-thirds of its promised cuts, which has raised concerns about Mazrouei’s credibility in trying to manage better compliance by others. Wearing its new hat, and under pressure from its long-time ally Saudi Arabia, the UAE is now expected to fully implement its pledged 140 kb/d cut, which would further strengthen the agreement.

Collectively, Venezuela (-200 kb/d), Mexico (-110 kb/d), Iraq (-100 kb/d), and the UAE (-100 kb/d) could potentially push the group’s supply lower by some 500 k/d in 2018 from average 2017 levels – provided other countries don’t increase production above their targets and offset the reductions. Moreover, Saudi Arabia has signaled it intends to keep production at below quota levels again in 2018, regardless if other countries improve compliance. Sharper production cuts may temper fears of a surplus in the first quarter, hasten the rebalancing of markets, and keep a floor under prices.

Much Ado about Nothing

Leading up to the Vienna conference, reported cracks in the strong Saudi-Russian alliance rattled markets and led to speculation that Moscow may force an early retreat from the pact. Unlike most OPEC countries with state-owned oil companies that must follow the dictate of their governments, Russian oil companies operate more independently and have chafed at the new production constraints. Novak holds regular monthly meetings with the dozen or so major oil companies that produce the bulk of the country’s production; in effect, he manages his own small OPEC-like group of companies to ensure a consensus.

Leading up to the meeting, Russia was apparently seeking a short time frame for the extension and pushing for a discussion of an exit strategy from the cuts, in contrast to Saudi Arabia’s stated position the deal should remain in place for all of 2018. The differing positions between the normally in-sync powerbrokers reflected their divergent views on the outlook for the pace of the market rebalancing next year and Russian fears that a continued rise in oil prices would trigger an avalanche of new shale oil supply. In the end, the agreement essentially reflects a compromise between the group’s de facto leaders, with the formal extension to the end of 2018 but with the June review just three months after the agreement was supposed to end in March. The deal was always going to be reviewed at the regularly scheduled June OPEC meeting anyway but subtle language in the press release enabled both sides to declare victory.

Dismissing market speculation of a potential breakdown between the two heavyweights, Falih, with Novak on his right, said in the briefing: “You can’t find light between us, we have been united shoulder to shoulder,” adding, “We are completely aligned.”

The Known Unknowns

The outlook for non-OPEC supply increases, global oil demand growth, and stock levels in 2018 was the main focus of the market monitoring committee in its deliberations the day before ministers convened the formal conference. Though the conclusions were not made public, it appears the group favored a more optimistic scenario judging by the communique. Fueled by sustained healthy economic growth, robust global oil demand has led to higher revisions since May, with it now projected to increase by just over 1.5 mb/d in both 2017 and 2018. OPEC’s internal analysis reportedly concluded that stockpiles would be back in line with the five-year average at the end of the third quarter or start of the fourth quarter of 2018, in contrast to other forecasts that see inventories rising next year, not declining.

Despite a razor-sharp focus on the outlook for U.S. shale production growth and its potential to upend the market impact of the agreement, a wide range in forecasts remains. Exceptionally, OPEC convened a technical level workshop on the outlook for shale oil production in 2018 the week prior to the ministerial conference. While OPEC officials did not provide details of the closed door workshop, conflicting presentations from experts from the United States reportedly added little clarity. Production projections range from 600 kb/d to as much as 1.4 mb/d, with a consensus coalescing around 1 mb/d, more than double the annual increase of 400-450 kb/d projected for 2017. For its part, the OPEC Secretariat is forecasting U.S. tight oil production at the much lower end of the range, which many analysts believe is too conservative.

Pragmatism Wins the Day

The strength of the Vienna pact exceeded market expectations, with a number of investment banks signaling a vote of confidence in the agreement by raising their price forecasts to a higher $54-62/bbl range for 2018. That compares to current year-to-date levels for international Brent of around $54/bbl and WTI of about $50.35/bbl. The corresponding increase in OPEC revenue will likely reinforce the group’s continued cooperation and commitment to production targets.

While uncertainties abound, the group’s commitment to stay the course with production cuts in 2018 and its proactive, pragmatic approach to a rebalancing of oil markets is expected to provide a foundation for prices going forward. However, there is little doubt that should shale surprise to the upside or demand disappoint to the downside the coalition will be forced to make good on its pledge to remain “agile and responsive” to market conditions.

The views represented herein are the author's or speaker's own and do not necessarily reflect the views of AGSI, its staff, or its board of directors.

As Gulf states reconcile fossil-fuel dependency with a transition to low-carbon energy systems, success will depend on their ability to integrate technology, carve out strategic market positions, and implement robust carbon governance reforms – such as emissions tracking and enforcement mechanisms.

A substantial drawdown on global oil stocks is forecast for the fourth quarter amid record oil demand, accelerating the rise in oil prices to the $100 per barrel threshold.

Saudi Arabia extends steep “voluntary” production cut through August but a weaker-than-expected Chinese economic recovery weighs heavily on market sentiment.

OPEC+ supply cuts starting in May could aggravate an expected oil supply deficit in the second half of 2023 at a period of greater economic uncertainty.

Equally, with the OPEC meeting behind them, analysts have shifted their focus to the wide range of uncertainties underpinning the market outlook in 2018, and especially the upcoming seasonally weaker first quarter demand period. The scale of the U.S. shale supply response to recent higher price levels, the strength of global oil demand, and heightened political risk in major oil producing countries are the main uncertainties influencing oil market sentiment. Saudi Arabia’s Minister of Energy, Industry, and Mineral Resources Khalid al-Falih acknowledged a “number of variables that we cannot fix with certainty going into the new year.”

Equally, with the OPEC meeting behind them, analysts have shifted their focus to the wide range of uncertainties underpinning the market outlook in 2018, and especially the upcoming seasonally weaker first quarter demand period. The scale of the U.S. shale supply response to recent higher price levels, the strength of global oil demand, and heightened political risk in major oil producing countries are the main uncertainties influencing oil market sentiment. Saudi Arabia’s Minister of Energy, Industry, and Mineral Resources Khalid al-Falih acknowledged a “number of variables that we cannot fix with certainty going into the new year.” Venezuelan output in October hit three-decade lows in the wake of the severe financial crisis and U.S. sanctions, with output plummeting by 180 kb/d from January to October. The decline in Venezuelan production has accelerated in recent months following the imposition of new U.S. sanctions, with October output at 1.91 mb/d versus its quota of 1.97 mb/d, according to the International Energy Agency. Analysts expect Venezuelan production to fall by an additional 200 kb/d in 2018.

Venezuelan output in October hit three-decade lows in the wake of the severe financial crisis and U.S. sanctions, with output plummeting by 180 kb/d from January to October. The decline in Venezuelan production has accelerated in recent months following the imposition of new U.S. sanctions, with October output at 1.91 mb/d versus its quota of 1.97 mb/d, according to the International Energy Agency. Analysts expect Venezuelan production to fall by an additional 200 kb/d in 2018. Iraq’s noncompliance has also rankled OPEC officials this year but may now be a nonissue after civil unrest and the capture of the oil-rich Kirkuk region by Iraqi forces led to the shut-in of some 300 kb/d of production. Baghdad has increased southern exports to partially offset the loss from the north, with November output estimated at around 4.33 mb/d. Production is expected to remain at reduced levels close to the country’s target of 4.35 mb/d while Baghdad and Erbil negotiate who controls sales and revenue of northern exports to the Turkish port of Ceyhan on the Mediterranean. Baghdad is demanding that Iraq’s State Organization for Marketing of Oil handle all of the northern sales from the Kurdish region but so far there have been no serious discussions on the issue and the stalemate may continue for another six months, until after Iraq’s parliamentary elections in May. As a result, Iraq may be more compliant with its target in 2018, or at least in the first six months of the year.

Iraq’s noncompliance has also rankled OPEC officials this year but may now be a nonissue after civil unrest and the capture of the oil-rich Kirkuk region by Iraqi forces led to the shut-in of some 300 kb/d of production. Baghdad has increased southern exports to partially offset the loss from the north, with November output estimated at around 4.33 mb/d. Production is expected to remain at reduced levels close to the country’s target of 4.35 mb/d while Baghdad and Erbil negotiate who controls sales and revenue of northern exports to the Turkish port of Ceyhan on the Mediterranean. Baghdad is demanding that Iraq’s State Organization for Marketing of Oil handle all of the northern sales from the Kurdish region but so far there have been no serious discussions on the issue and the stalemate may continue for another six months, until after Iraq’s parliamentary elections in May. As a result, Iraq may be more compliant with its target in 2018, or at least in the first six months of the year.